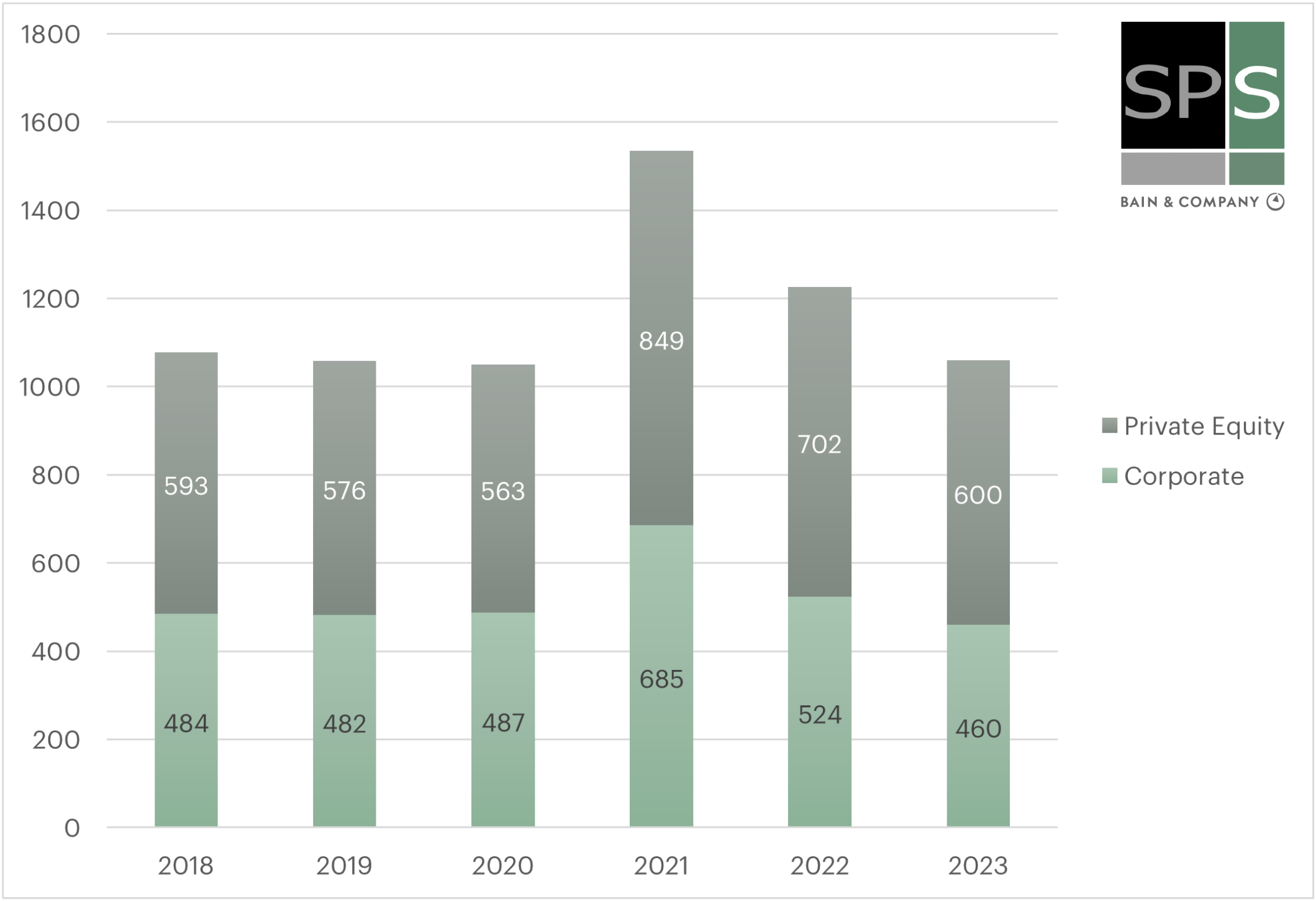

According to research from SPS by Bain & Co., healthcare M&A was already declining from heady levels of 1,534 deals in 2021 before the Federal Reserve started increasing interest rates to counter inflation last year. The total number of healthcare deals in 2023 was 1,060, a 15% decline from 2022, albeit only a slight decrease from pre-pandemic deal volume in the sector.

YoY Healthcare M&A Deals – PE & Corporate

Even so, Bain & Co’s Global Healthcare Private Equity Report 2024 reveals areas of potential opportunity: “We see positive momentum generated from innovation triggered by the pandemic, which has led to a range of new healthcare delivery models and modalities (such as remote physiologic and therapeutic monitoring, and at-home care), and new life-sciences capabilities (such as contract development and manufacturing organizations’ supply expansion and Covid vaccine distribution),” the report said.

No doubt, the overall M&A market in 2023 was stressed compared to the previous two years. Research from SPS reinforces a trend toward buy-and-builds as firms choose to bolster current investments rather than acquire new ones.

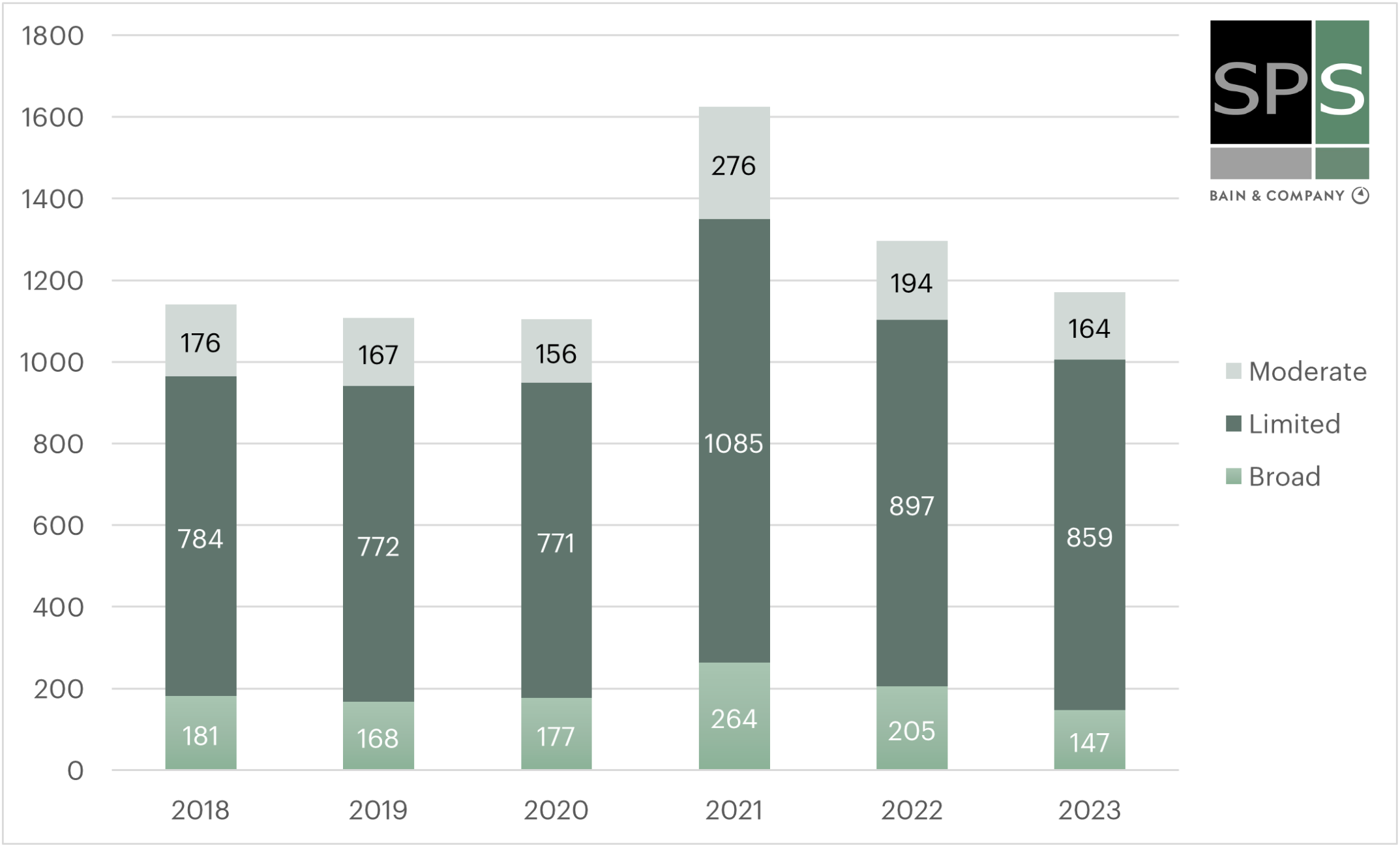

In 2023, the appetite for PE add-on deals in the healthcare sector was high compared to buyouts, indicating depressed valuations for assets at auction. Though activity in all deal types has declined over the last three years, in 2023 add-ons accounted for a considerably higher percentage of the total than they did between 2018 through 2020, at 430 add-on deals last year. That compares to 338 in 2018, with a similar number of total healthcare deals at roughly 600.

In keeping with the theme of small deals to enhance investments and avoid selling at low valuations, the portion of healthcare M&A deals that had limited auctions in 2023 was 73% – the highest it’s been in six years. In 2021, when healthcare experienced the highest M&A volume, limited auctions were 67% of the total, suggesting more robust sale processes that year.

YoY Healthcare M&A Deals by Sell-Side Process – PE & Corporate

Despite a dim account of 2023 healthcare activity, Bain’s & Co.’s report reflects a cautiously optimistic outlook on 2024 opportunities. “Inflation is cooling as the impact of higher interest rates take effect, while elevated material and labor costs are showing up as higher reimbursements for healthcare goods and services. In credit markets, rates are projected to remain elevated.

“We expect sponsor-to-sponsor and secondary transactions to increase in 2024,” said Bain. “Meanwhile, take-privates, carve-outs, and secondaries will continue to represent an elevated share of deal activity as investors seek to unlock value.”

Areas of opportunity lie in innovation from generative artificial intelligence and healthcare information technology; cell, gene and RNA therapies and antibody drug conjugates; and diversification into Asia-Pacific, especially India, according to Bain.

To sum, 2023 was a year of comparatively restricted M&A that favored small deals to bolster companies before a takeout. But there’s reason to believe 2024 will see growth in numbers of companies engaging in secondaries, carve-outs and privatizations.

To track and analyze recent years’ deal activity in your target sector, request an SPS demo today.