As private equity firms enter 2025, traditional deal-sourcing methods are no longer enough. The SPS 2025 Private Equity Harvest Report reveals critical insights into portfolio holding trends, evolving exit strategies, and shifting buyer-seller dynamics, helping firms refine their sourcing approach in a rapidly changing market.

“With a record supply of PE assets primed for exit, there’s no shortage of opportunity. Whether you’re a sponsor, strategic, lender, or advisor, viable deals are out there—if you know where to look.” — Brenden Gobell, Managing Director

The backlog of 7,400+ PE-backed companies still held from 2014-2021 acquisitions underscores the growing importance of strategic deal sourcing. With holding periods extending and sponsors re-evaluating exit strategies, firms that can identify high-quality, actionable assets will be best positioned to capitalize on this evolving market.

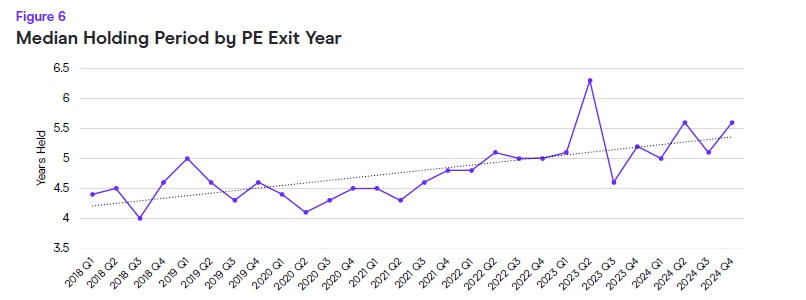

Holding Periods Are Extending—And Timing is Critical

The SPS 2025 Private Equity Harvest Report confirms what many sponsors already feel: holding periods are rising across the board. The average portfolio company is now held 1.15 years longer than in 2018, with upper middle-market assets now exceeding 5.5 years on average

Key drivers behind extended hold times include:

- Macroeconomic pressures – Interest rates and inflation have slowed deal-making.

- Valuation concerns – Sponsors are waiting for improved pricing before exiting.

- Operational value creation – Firms are prioritizing margin improvements, cost efficiencies, and organic growth.

At the sector level, Industrials and Consumer businesses are experiencing longer holding periods, while Technology and Healthcare assets are cycling through faster due to sustained demand. Despite these differences, one key question remains: How do sponsors recalibrate their sourcing strategies in a market where traditional exits are no longer guaranteed?

Where Are PE Firms Looking for Deals?

This trend is particularly evident in Industrials, where sponsors remain the primary sellers in middle-market transactions. Meanwhile, in Technology, 72% of acquisitions are coming from private companies, largely through venture capital-backed firms. The data is clear: firms seeking quality deal flow should focus on high-growth, privately held companies, particularly in Technology, Healthcare, and Renewable Energy.

Watch the insight clip from our recent webinar:

Creative Exit Strategies: Secondaries & Sponsor-to-Sponsor Deals

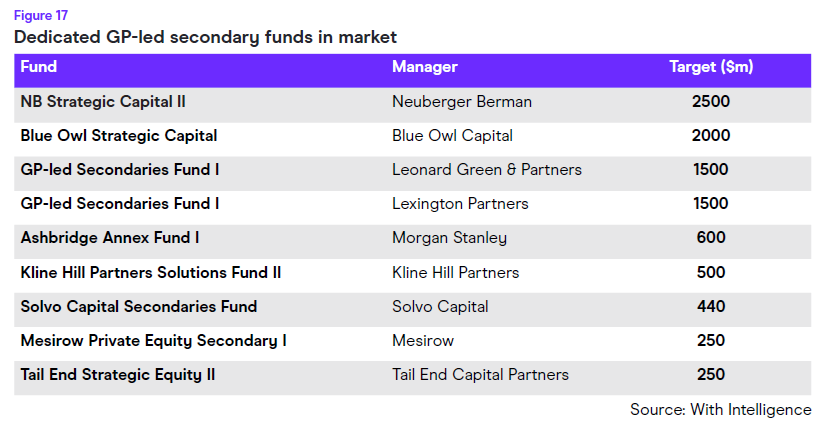

With extended hold times and evolving exit strategies, firms are increasingly relying on GP-led secondaries and sponsor-to-sponsor deals to transition assets.

- GP-led secondaries now account for 50% of total secondary market volume, enabling firms to:

- Retain high-performing assets while preparing for future exits.

- Extend holding periods while maintaining portfolio flexibility.

- Access liquidity in a challenging M&A environment.

- Sponsor-to-sponsor deals remain a critical exit strategy, particularly in Industrials and Business Services. These transactions allow firms to:

- Move aging assets more efficiently.

- Refinance and restructure portfolios.

- Acquire well-managed businesses with add-on potential.

For firms sourcing sponsor-backed deals, tracking these movements is key to identifying high-quality, actionable assets before they formally hit the market.

Looking Ahead: Smarter, Data-Driven Deal Sourcing

With a record backlog of PE portfolio holdings, the market is shifting. Firms that leverage data-driven sourcing strategies—whether through secondaries, sponsor-to-sponsor transactions, or proprietary outreach—will be best positioned to capitalize on where deals are emerging next.

Download the full 2025 Private Equity Harvest Report to sharpen your sourcing strategy.