As private equity firms recalibrate sourcing strategies for 2025, the middle market stands out as a sector of renewed interest and untapped opportunity. Often overlooked in favor of larger transactions, middle-market assets are proving to be not only more resilient but also highly actionable for firms seeking scalable growth with manageable risk.

The 2025 Private Equity Harvest Report reveals that this segment is increasingly central to sponsor activity, particularly as firms contend with longer holding periods, shifting exit strategies, and the need for targeted deal flow. The full report offers deep insights across all key market segments; below, we analyze portfolio activity trends in the middle market.

Why the Middle Market Matters Now

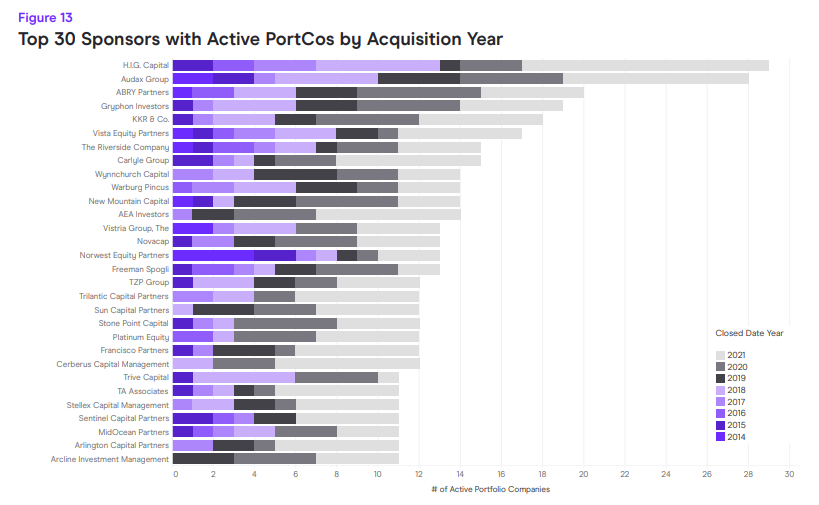

Private equity firms are holding onto assets longer than ever, and the middle market is no exception. Many sponsors in this segment still hold assets acquired in 2015 or earlier—Norwest Equity Partners, for example, holds a majority of its active portfolio from 2017 or prior. This longevity suggests a measured, long-term approach and highlights the potential for near-term exits as firms look to rebalance portfolios.

Between 2014 and 2021, the ratio of add-on acquisitions to buyouts surged to 2.5:1, highlighting a preference for scaling existing investments. This shift speaks to the middle market’s growing importance, as firms are increasingly finding value in companies that are neither too large to be unwieldy nor too small to lack scalability.

Moreover, the gap between lower and middle market holdings is narrowing, indicating a broader shift in how sponsors are constructing their portfolios and targeting growth-stage companies. This segment offers fertile ground for implementing operational improvements, driving profitability, and achieving strategic growth.

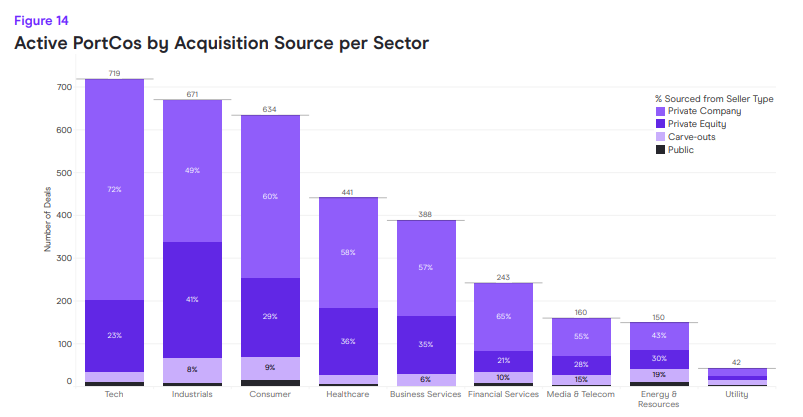

Seller Dynamics Vary by Sector

What sets the middle market apart is the diversity of deal origination sources:

- In Industrials, sponsors remain the dominant sellers—suggesting a strong pipeline of sponsor-backed, institutional-quality opportunities.

- In Technology, 72% of acquisitions are sourced from private companies, often venture-backed—making it a highly dynamic space fueled by innovation and growth potential.

This variability in seller type points to the need for tailored sourcing strategies across sectors within the middle market.

Strategic Considerations for PE Firms

Embracing the middle market necessitates a nuanced approach:

- Operational Value Creation

- Middle-market companies often present opportunities for margin expansion through focused operational improvements—without the complexity and overhead of larger enterprises.

- Flexible Deal Structures

- Given the range of seller profiles, from family-owned businesses to VC-backed start-ups, firms must adapt their approach to align with founder dynamics, growth expectations, and risk profiles.

- Long-Term Partnership Models

- With many assets held long-term, successful sponsors are those who invest deeply in management alignment and pursue strategic growth over rapid flips.

The Takeaway

As PE firms face a growing backlog of aging assets and a highly competitive deal environment, the middle market emerges as a strategic sweet spot—rich in opportunity, yet requiring nuance in approach. With the right sourcing strategy and execution model, firms can unlock meaningful value in this segment.

The full 2025 Private Equity Harvest Report explores these trends across all market segments—download it to discover where your next opportunity may lie.