New rules of the game— Dealmaking in the Fed’s new regime

Since last year, PE firms have taken a step back from closing deals. Following the deal boom of 2021, many firms enjoyed a prosperous fundraising period. But even with pockets full of dry powder, firms have been reluctant to capitalize given a flurry of global and economic headwinds.

Instead, firms have assumed a conservative approach in preparation for all eventualities: Will the Fed keep raising rates? Will inflation cool? Are we looking at a hard or soft landing?

These uncertainties have had a tightening effect on investment strategy, and many business segments are feeling the burn. Unsure of the rules of the game in early 2023, PE firms have sidelined demand for new deals and practiced risk aversion to a greater degree, causing a slowdown in deal activity until equilibrium is signaled.

That first signal may have come in late August, when Chair Powell indicated the Fed’s plan to maintain its official interest rate at a restrictive level to combat the possibility of entrenched inflation, but to avoid further escalation as long as conditions permit. This position was upheld in its late September decision to hold off on a rate hike.

Though commitment to a restrictive rate policy is suboptimal for M&A market conditions, predictability creates the opportunity to be proactive. With new considerations, PE firms may be ready to increase activity now that the outlook on interest rates has settled into a steady, albeit less attractive, order. Half-time is over, the game can start again – but with a new set of rules.

Some firms have been chomping at the bit to start getting deals done. On a late July webinar sponsored by SPS, Don McDonough, Managing Director at GTCR said, “We’re fortunate to have two new funds with a lot of dry powder that we’re looking to deploy…We’re eager to put it to work and are trying to lean into the market. The challenge is finding that equilibrium with the sellers.”

Tom Aronson, Vice Chairman and Head of Originations at Monroe Capital, repeated the sentiment, noting, “Everyone’s looking to do deals…but from a debt perspective, we have a little bit more scrutiny in the types of deals we’re willing to provide debt to.”

So, where are firms looking to put this capital to work? Professionals have been pointing to a decent level of deal flow so far this year, but high competition for very few assets in segments that have exhibited economic resilience, like fire and security services.

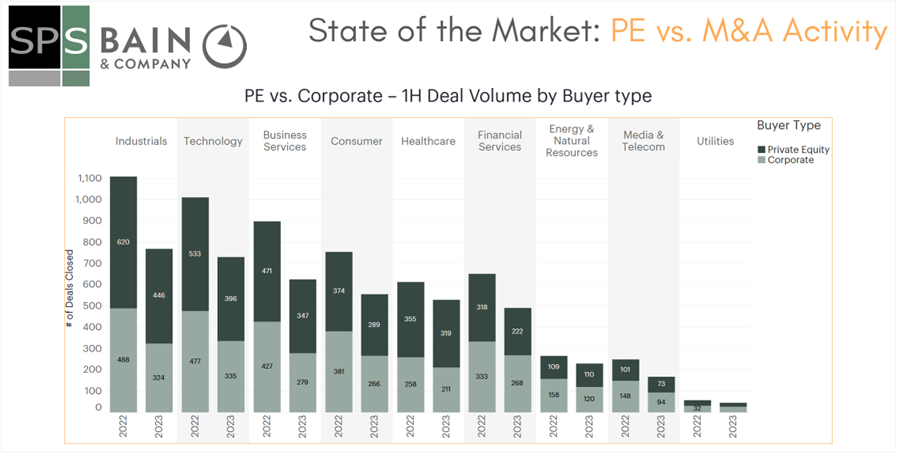

According to our data, Industrials, Technology, and Business Services had the highest deal counts in 1H 2023.

Beyond the sector focus, with the cost of capital remaining relatively high, firms are being careful to select companies with strong debt profiles.

Here are some of the key attributes that comprise an economically sound M&A investment in this environment:

- Costs: Firms are evaluating key inputs like supply chain, labor, and energy-related costs, and how they’ve been affected over recent years by the pandemic, war in Ukraine, and other macro events. Companies whose inputs are more insulated from price fluctuations will be more attractive to investors until demand and supply steady.

- Leverage: With decreased risk tolerance, firms are more wary of highly leveraged assets and the impact of financial downturn on their ability to service the debt.

- Fixed-charge coverage: A high fixed charge coverage ratio signals a healthy ability to cover financial obligations with operating income, and in turn, lower financial risk to investors.

While many PE firms already know what they’re looking for in this new regime, with quality of deal flow down, sourcing for assets that fit the bill is becoming increasingly difficult. Winning deals in this market may be a function of adopting new, alternative, or data-driven deal sourcing mechanisms.

By leveraging technology-enabled levers, PE and M&A firms can combat the competition by leaving no stone unturned. Partnering with SPS enables investors to uncover companies hiding in niche sub-industries, ones that went under the radar with broken processes, or even sponsor-owned assets that refinanced before rates peaked and are ready to trade again.

PE firms won’t sit back on deep pockets forever, and now with a glimpse into the foreseeable future, deal activity has the potential for a strong comeback in 2024 – but will look very different. Origination strategies will need to adapt – becoming more purposeful, comprehensive, and informed – to compete.