The PE market has regained some footing compared to the first half of 2023. With GPs’ new year resolutions to deploy large sums of capital accumulated during recent fundraising cycles, funds are now tasked to find good deals and create value for their LPs.

As indicated by an early 2024 SPS market analysis, PE exits accounted for over a quarter of new platform acquisitions closed by sponsors over the past five years, and over 60% of PE exits went to PE buyers in the same period. In a difficult deal sourcing environment, direct to sponsor sourcing has proven to be a worthwhile investment strategy in recent years.

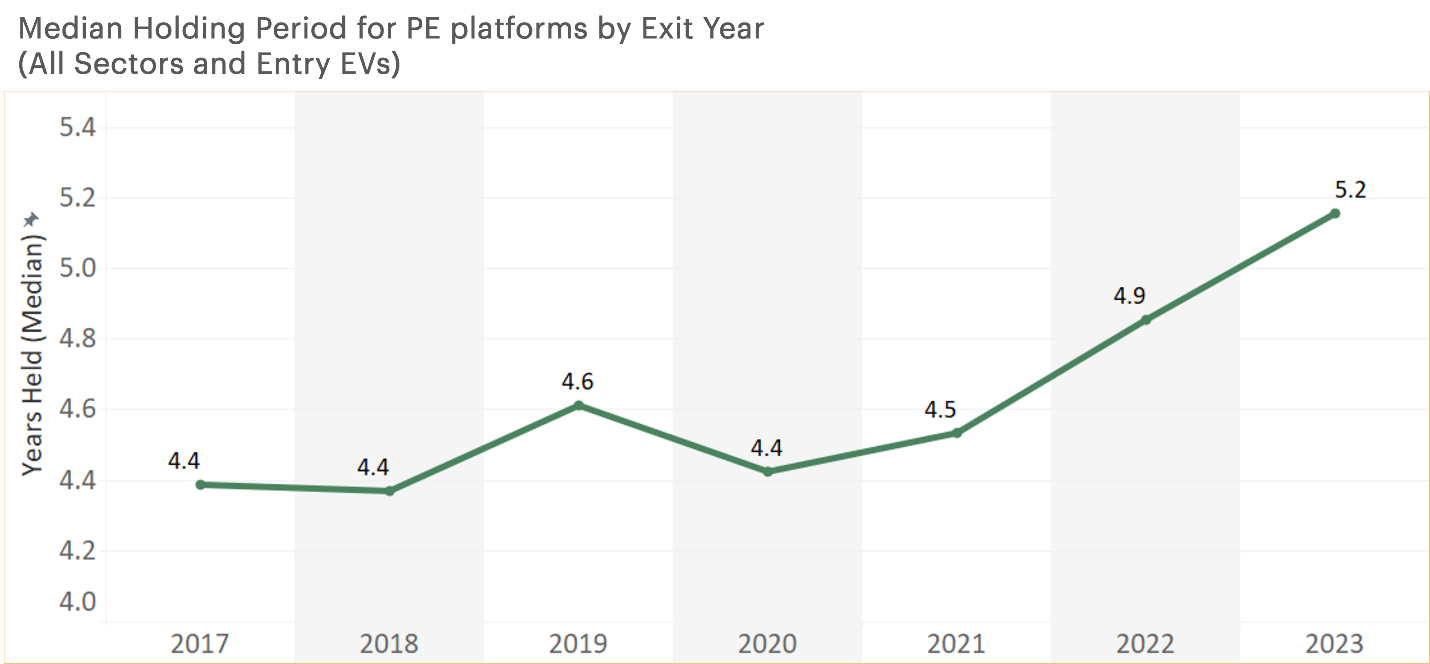

There’s one major roadblock to finding these deals now: the higher-for-longer interest rate environment has brought a prolonged reluctance to sell, obstructing abundant deal flow. A key indicator of this sentiment, extended hold periods for PE-owned assets have become the norm. According to our data, the median holding period for PE exits in 2023 was 5.2 years, up from 4.5 in 2021.

Naturally, funds have remained averse to selling in a market riddled with uncertainty over the past year. Given the high cost of capital, “sellers are not interested in selling at the lower prices needed to make buyers’ deal models work…the current owners of the businesses are sitting on credit agreements that they can’t replicate in today’s market,” notes Hugh MacArthur, Chairman of Global Private Equity Practice at Bain & Company.

But sellers’ obstinacy does not come without its own risks:

- Just as borrowing rates have risen, so have refinancing rates. According to MacArthur, “With average loan durations, many of the companies still being held will need to refinance their debt at rates that look like 12% and not 5%. For those companies that still have material debt, the sellers now face the same situation as buyers.”

- Exit backlogs could weigh down overall fund profiles. Some sectors have taken serious hits on generated returns during volatile market conditions over recent years. With value creation being the name of the game, longer hold periods may not be able to sustain long-term fund performance goals.

- Changing industry trends may impact performance. The longer companies are held, the more funds risk scrutinization and strain on their portfolio companies based on evolving macro trends, such as cybersecurity concerns, disruption from AI, or ESG guidelines.

With data on our side, we can see the bright side of the constrained exit environment. According to a recent analysis from SPS’ Private Equity Harvest Report, there are over 5,100 companies that originally traded to PE investors between 2012-2019 that are still being held.

Aged assets coming to market is an eventuality, and our evaluation of current and historic PE holding periods indicates a surge of relevant target acquisitions in the months and years ahead. When they do come to market, PE firms need to be ready with a strategy to source from other sponsors, while firms that already focus on secondary buyouts are ahead of the curve.

The PE Harvest Report reveals these often-overlooked opportunities, analyzing the current landscape of PE portfolio holdings through several strategic lenses:

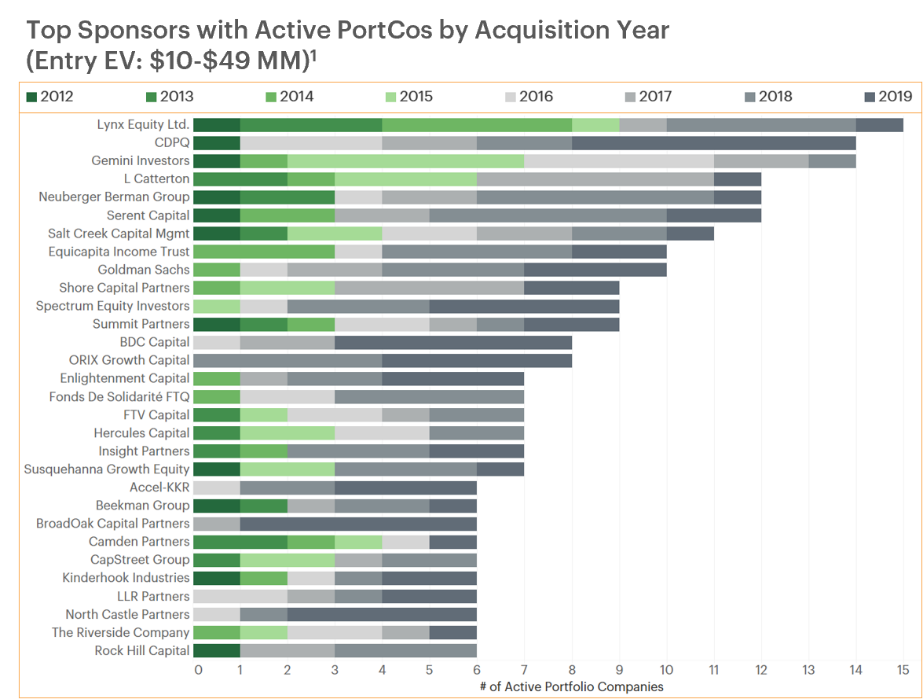

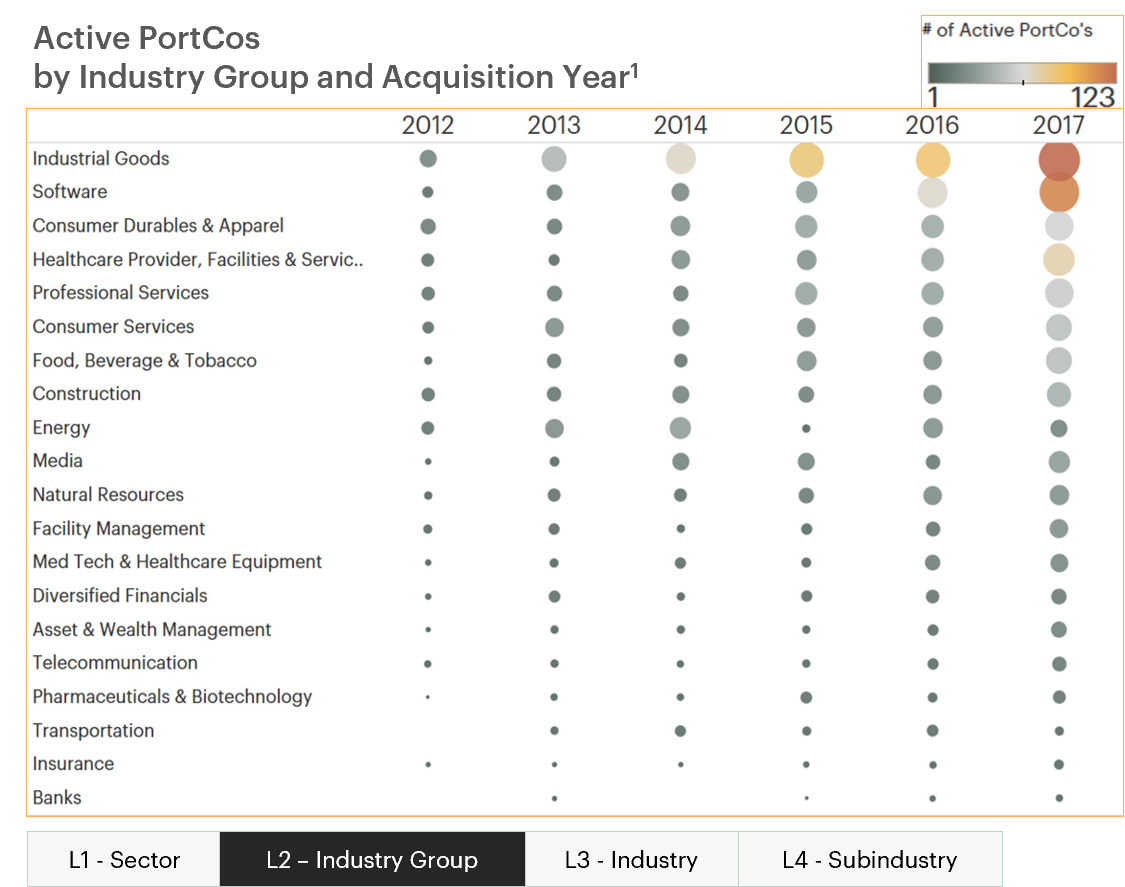

Strategy 1 – Lower Market: As deal activity slowed by 19% from 2022 to 2023, lower market-focused funds are increasingly opening their strategy to buy from other sponsors, sometimes seeing second chances on attractive deals. Below are the top sponsors with active portfolio companies by acquisition year:

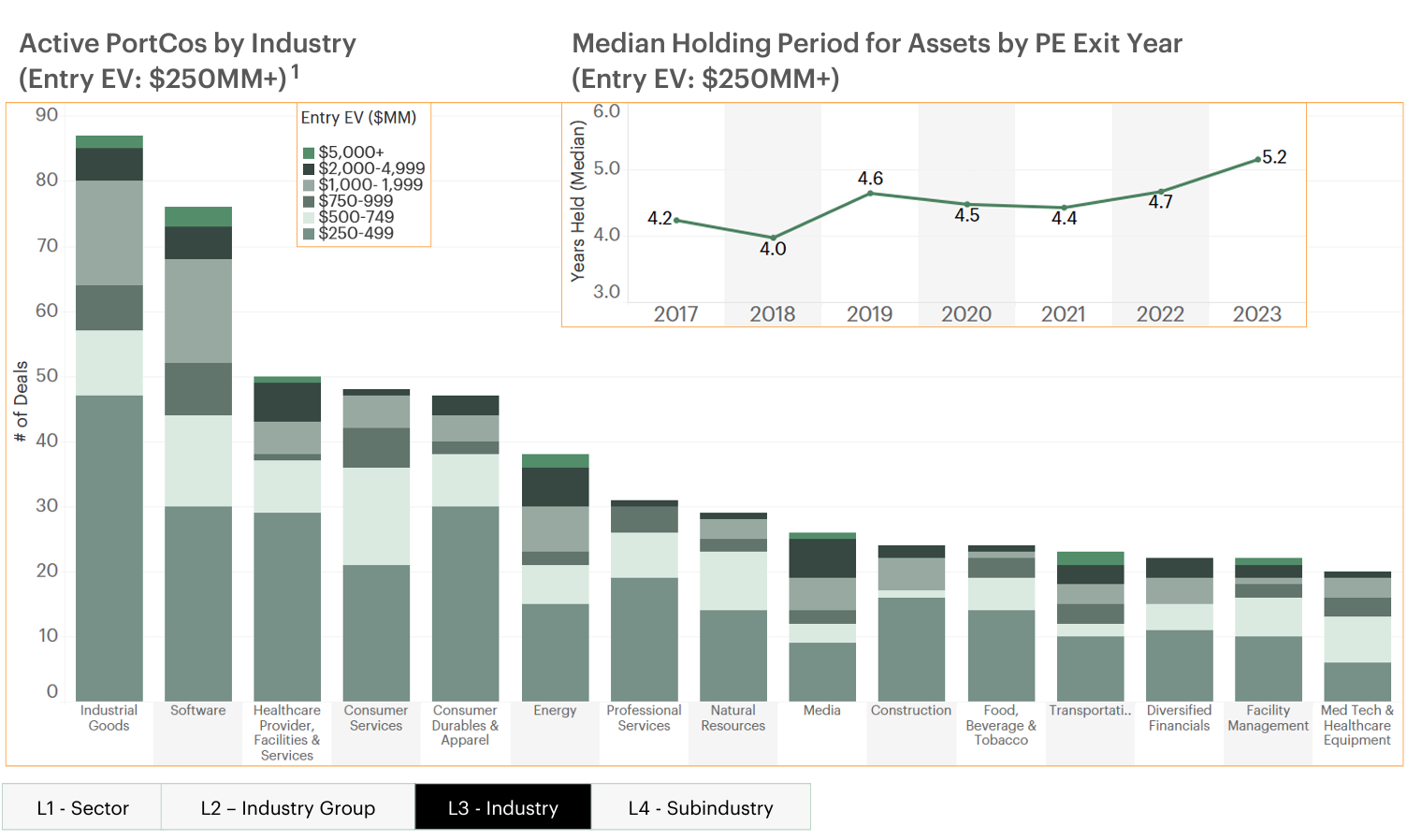

Strategy 2 – Upper Market: The median holding period for PE assets with entry EVs above $250MM in 2023 was 5.2 years, up from an average of 4 years in 2018. The chart below shows active PE portfolio companies with larger entry EVs by Industry, and the median holding period for these assets by PE exit year from 2017 to 2023.

Strategy 3 – Minority Investments: Amid seller reluctance and a suboptimal time to transact, minority investment strategies are an attractive alternative for PE investors.

Strategy 4 – Stranded Assets: Some firms are getting creative with their sourcing tactics, taking stock of active companies with extended holding periods to reveal distressed assets, growing assets in need of additional capital, or attractive assets that have demonstrated economic resilience through hard times.

Holding periods have already reached unprecedented highs, and funds have an ultimate goal to monetize. The bottom line is: exit activity can’t stay stagnant and something needs to give. Some portion of those longer-held assets are guaranteed to come to market in the coming quarters, with a likelihood of some sellers compromising on price. Be ready when they do, with the help of SPS.