SPS by Bain & Co.’s 2024 Deal Sourcing Databook has captured the highs and lows of private equity activity in the last five years, from doldrums in the first year of the COVID-19 pandemic, to heady activity from pent-up demand the following year to another slouch once central bank rates began rising in 2022.

Key revelations from the report include a deep dive into the constrained exit environment, as holding periods for private equity-owned portfolio companies reached a record high of five years in 2023. SPS also found that the portion of deals sourced by PE firms that end up closing has significantly declined, resting at an average of approximately 24% in Q1 2023, compared to historical averages between 30% to 40%.

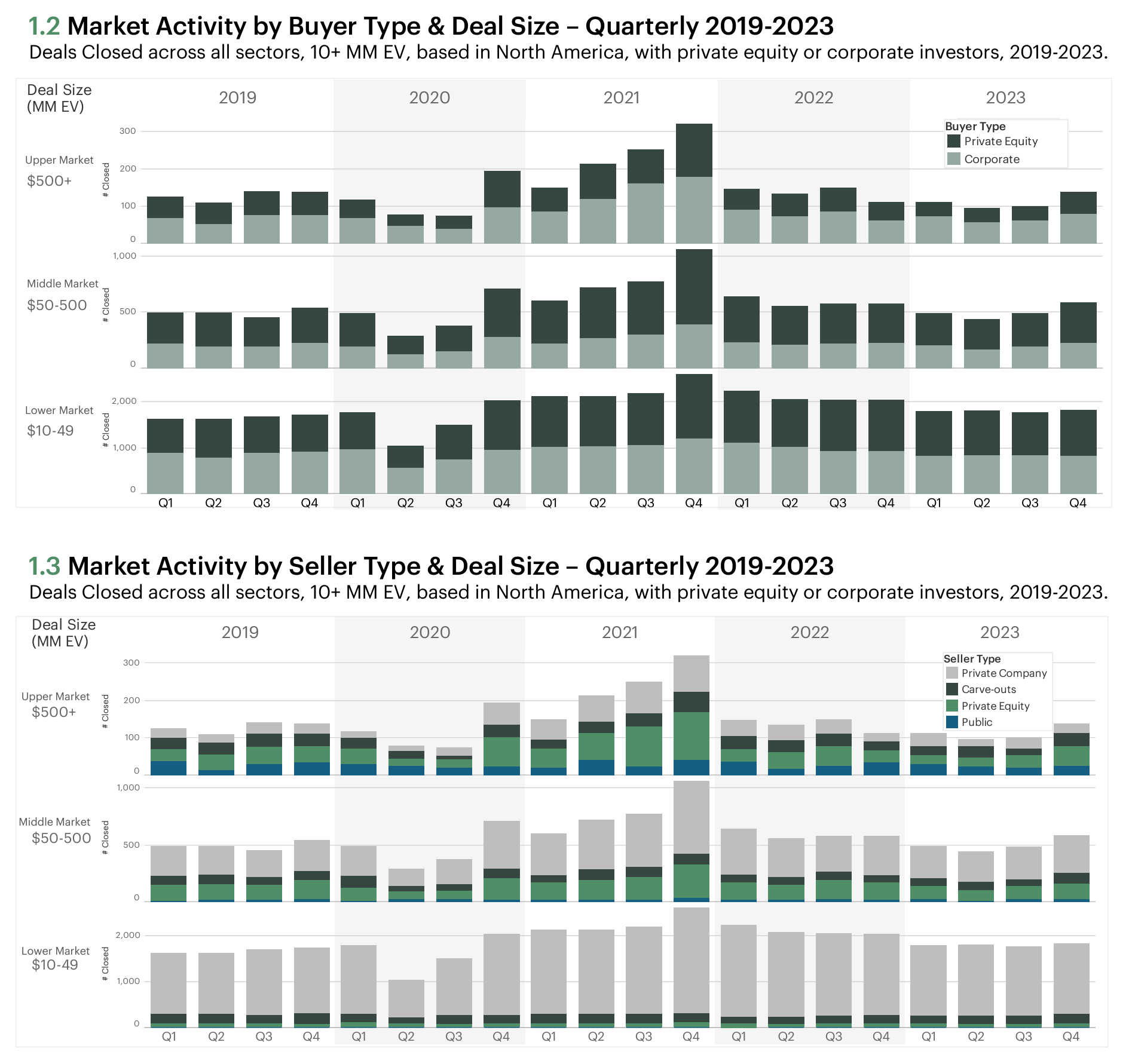

Firms in the Middle Market segment, defined by SPS as transactions in the $50 million to $500 million enterprise value (EV) range, drive a substantial portion of overall deal activity. Deal volume in this size range slumped in 2022 as the FED increased interest rates, the economy slowed, and a disconnect emerged between buyers and sellers on valuations. The last couple of years, however, have seen a modest improvement over pre-COVID 2019 levels, especially in Q4 2023 with deal activity at an 8% increase from Q4 2019.

Between 2019 to 2023, private equity investors have been the primary source of Middle Market buying activity, while most sellers in the middle market were private companies, followed by private equity firms and a small share of carve-outs of larger companies.

As PE has found ways to continue deal-making in the stressed valuation environment of recent years, add-ons represented the highest share of total market deal activity during this period, though not all PE firms engaged in buy-and-builds to the same extent.

Most deals in the Middle Market were platform buyouts from 2019 to 2023, with a minority of deals being add-ons and financings, compared to add-ons representing a roughly equivalent share to buyouts in the Lower Market ($10 million to $49 million EV). Continuing with the theme of smaller deals bolstering Middle Market M&A, in 2022 and 2023, financings were also on the rise.

Most Middle Market deals fell into the Software Industry Group between 2022 and 2023, followed by Industrial Goods and Healthcare Provider, Facilities & Services. Most industry groups see broader processes relative to limited and moderate auctions in this size range, with Software as a notable exception with greater variance in terms of sell-side process competition.

With brimming dry powder estimated at $3.2 trillion globally according to Bain & Co., PE is faced with the challenge of generating liquidity sooner rather than later. And because deal size is relatively modest in the Midde Maret, assets in this size range have the advantage of requiring less leverage at more reasonable valuations than larger assets. But due to continued high interest rates, it remains to be seen if bullish expectations at the beginning of 2024 will pan out in the end.