The timeline to close a private equity deal has become a critical metric for stakeholders. As market conditions fluctuate, this Time to Close (TTC), or the time between a deal being initially logged in a firm’s pipeline to a completed transaction, has lengthened, impacted by a confluence of economic factors. Through the lens of SPS’ proprietary analysis of PE pipeline data, we explore trends from recent quarters to understand how the closing timeline has evolved and what it means for PE investors and sellers.

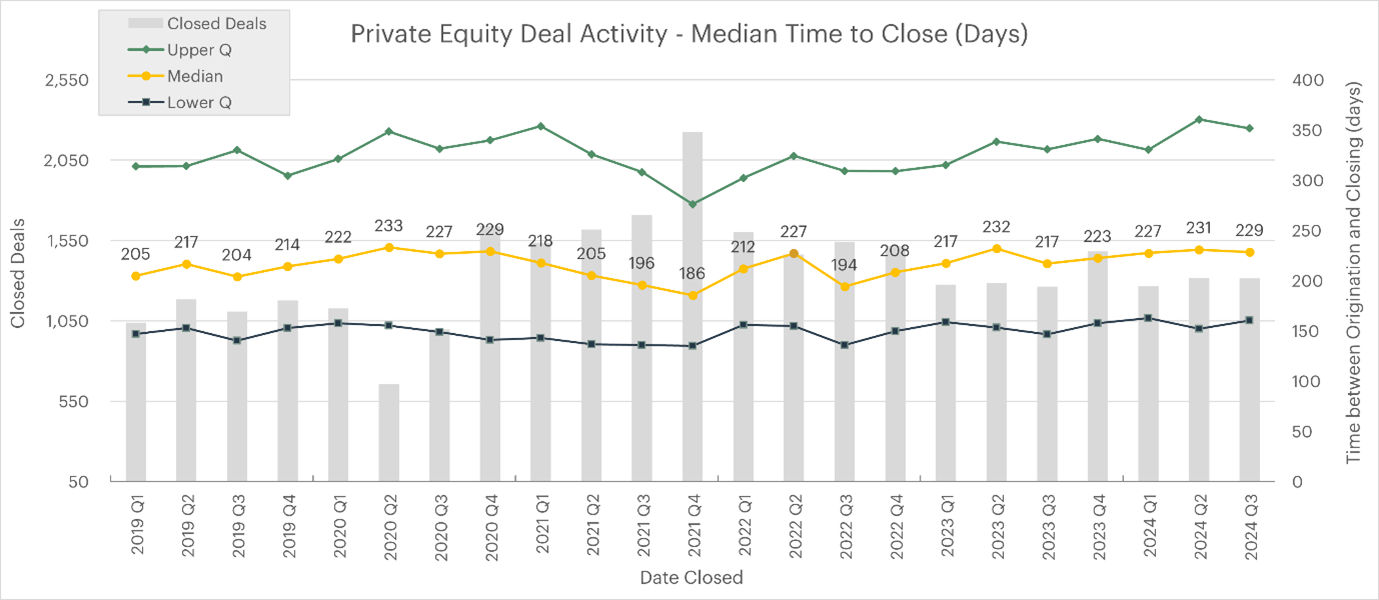

For PE deals completed in Q3 2024, the median TTC was 230 days – a steady increase from the 194-day median seen in Q3 2022. This consistent upward trend suggests that deals are taking longer to reach completion, with market factors continuing to introduce new challenges and delays.

TTC – ALL DEAL SIZES

As we look back at PE deal activity, 2021 stands out like a neon sign. This was a year of deal-making at a frantic pace, with PE firms eager to make up for lost time after the pandemic slowdown. That year saw a record number of deals coming to market, creating what we might call a “deal traffic jam” to work through. As pent-up demand poured into the market, every stage of deal-closing faced pressure, setting a precedent that affected closing times even after things cooled down.

Although the timeline has stabilized somewhat from the peaks of 2021, slight increases indicate ongoing complexity in the deal-making process. As private equity firms evaluate today’s opportunities, they’re wondering how much longer it might take to get deals across the finish line compared to those high-velocity days of 2021.

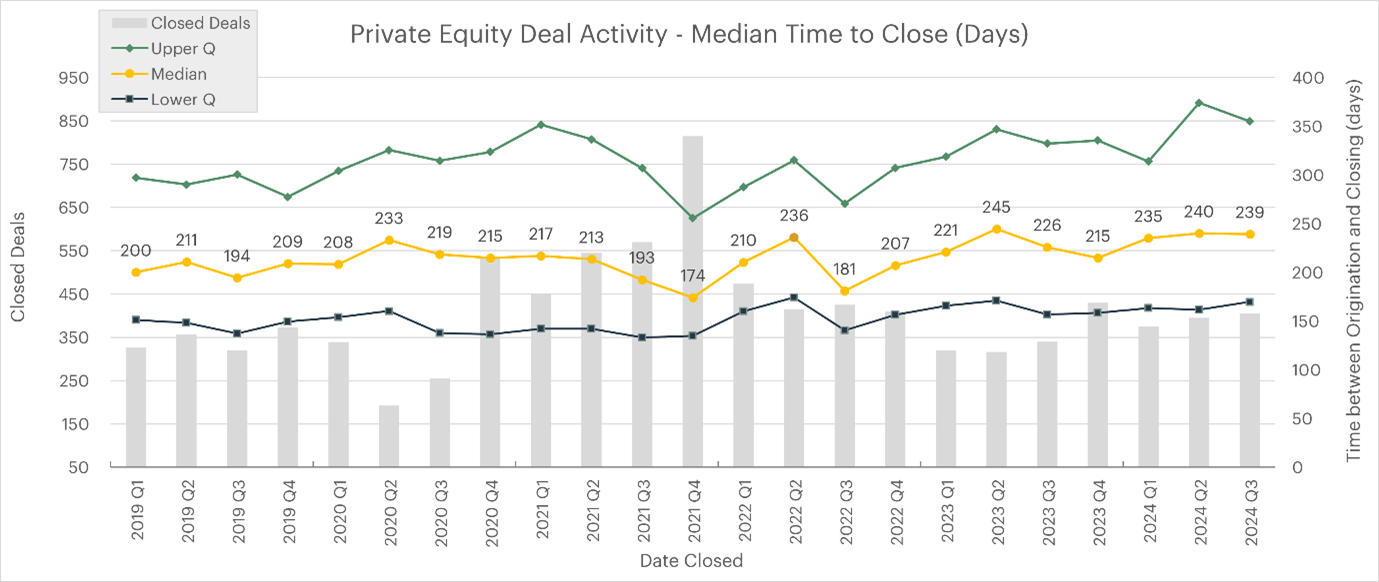

Interestingly, the disparity in closing times between smaller deals and larger ones is growing. When excluding smaller transactions (under $50 million EV), timelines tend to be more volatile for larger deals, which are more susceptible to external factors like debt financing. Deals involving larger firms—often with complex debt structures and more stakeholders—tend to have lengthier and less predictable closing processes.

TTC DEAL SIZES 50+

Market conditions, economic uncertainty, and financing challenges are all factors forcing dealmakers to rethink timelines, sometimes dragging them out to unforeseen lengths, particularly in high-value acquisitions. While smaller deals may close more predictably, mid-to-large transactions are often delayed by financing hurdles, negotiation complexity, and sometimes even regulatory factors. In contrast, smaller deals tend to move faster, largely unaffected by debt fluctuations that influence high-value transactions.

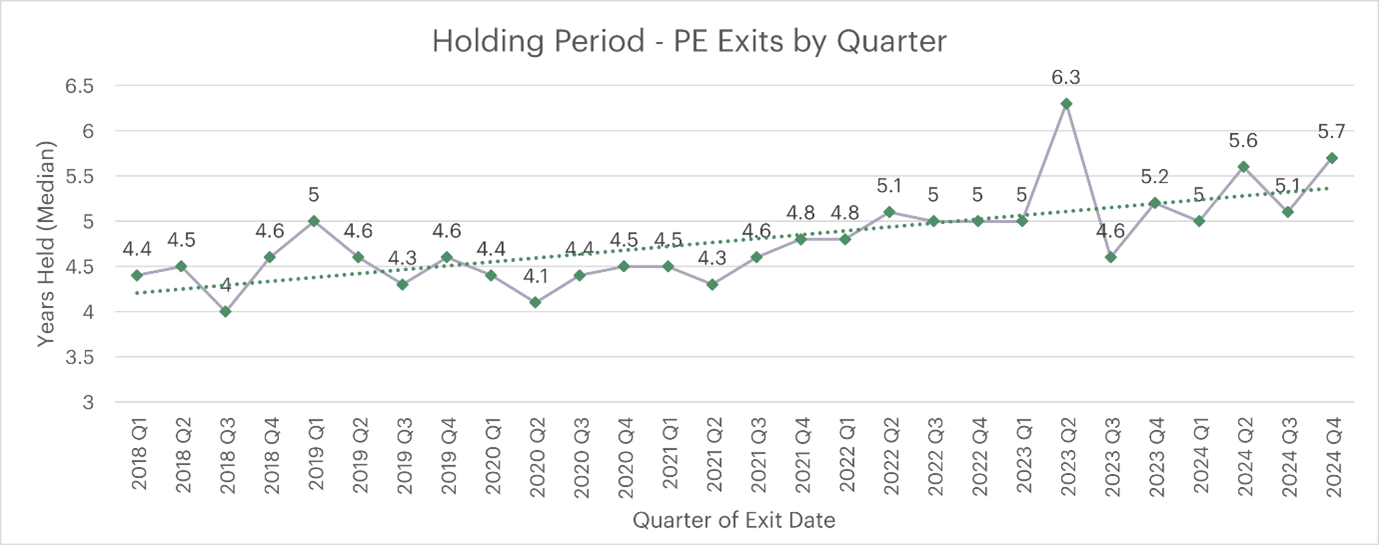

Another factor influencing the PE market dynamics is the holding period, or the length of time a private equity firm retains an asset before selling it. In Q3 2024, SPS PE Harvest data suggests that longer holding periods correlate loosely with closing times, with assets held over extended periods often taking longer to sell. Many PE firms face “deal fatigue” due to elongated holding periods, partially due to the challenging exit environment.

HOLDING PERIODS

The increased TTC is becoming a defining characteristic of today’s private equity landscape. By keeping a pulse on these timelines, private equity firms can better anticipate market shifts and adapt their strategies, focusing on efficiency in due diligence and carefully managing financing.