Recent years’ events have given us in the M&A deal sourcing world a sort of whiplash not previously encountered. The steady growth of deal activity over the past decade has been suspended, with the initial pandemic drop giving way to soaring levels through 2021. That boom has been punctuated by looming threats of a decline induced by today’s turbulent economy, supply chain shock, rising inflation and interest rates, and geopolitical tensions – to name a few contributing factors.

Investors are meeting these mounting uncertainties with preparation for various downturn scenarios – a wise move given historical inflation-recession patterns, as cited in Bain & Company’s Private Equity Report – Midyear 2022. Yet, recent history has revealed some degree of insulation of private equity deal activity from macro trends, with some verticals like Services, IT, and Healthcare sectors enduring the COVID lull with robust closing volumes, according to SPS data. With all the discourse surrounding today’s economic environment (Are we in a recession? If yes, why is this recession different?), the real question remains: Is this a healthy investment environment for private equity?

The outlook for deal activity during the current period of uncertainty may not be that bleak. During our latest deal sourcing webinar, Sharpening Your Sourcing Strategy in Anticipation of a Down Market, Kathryn Cesari, Director of Financial Sponsors Group at William Blair said of the advisor side, “We have a robust pipeline, we still have a lot of deals to launch in the back half of this year…things are looking cautiously optimistic.” Brad McGowan, Head of Financial Sponsor Coverage & Deal Origination at Pickwick Capital Partners echoed this sentiment, as have many across the M&A world at large.

Here’s the case for why investors may have reason to remain hopeful for deal closings against the backdrop of a volatile threat landscape:

PE is Resilient

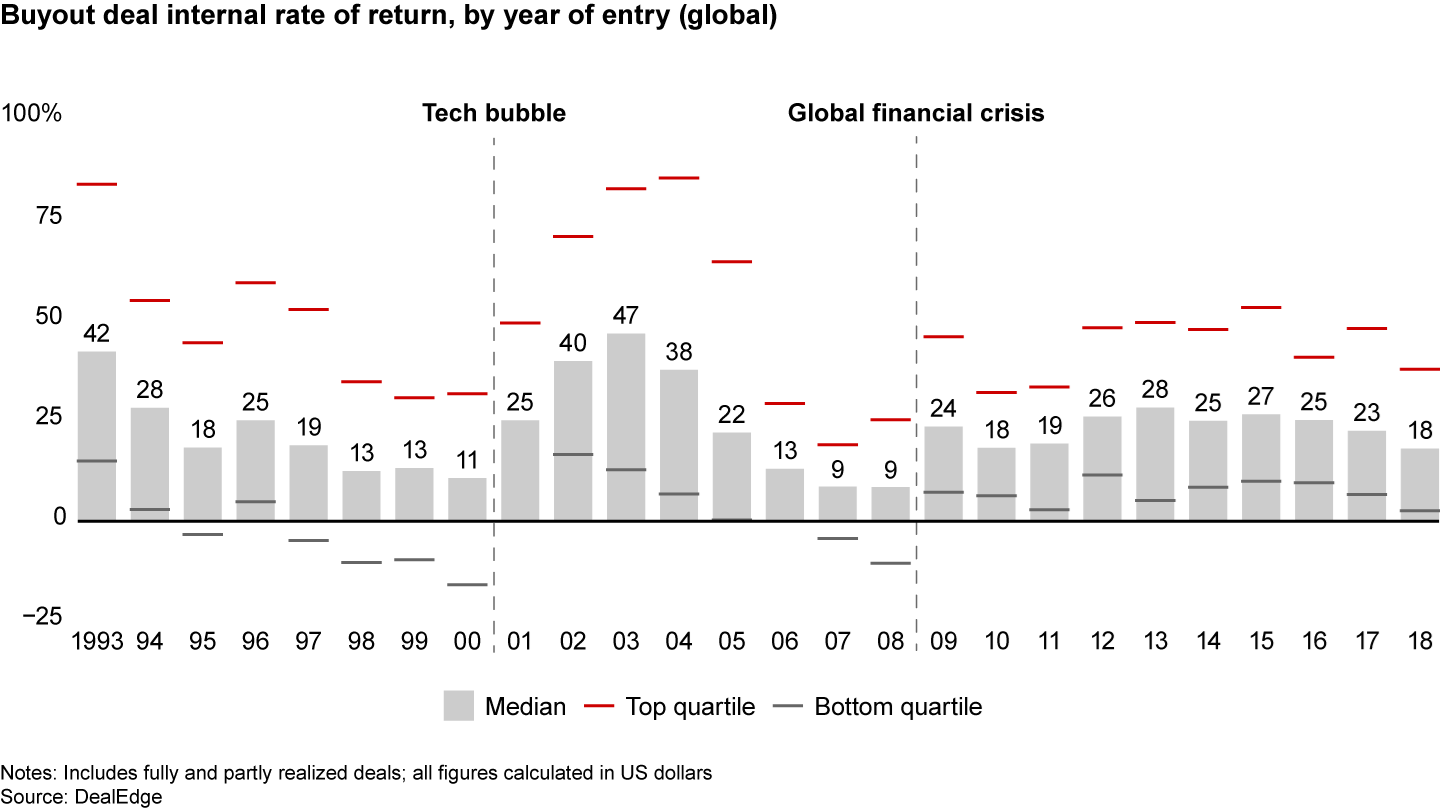

Not ones to sit out a good fight, PE has been historically resilient in mitigating hard times, typically delivering strong returns following recessionary cycles. Take this research conducted by DealEdge, a Bain & Company venture offering deal performance analytics. As cited in Bain’s mid-year report, “The IRR from investments made during recovery years has consistently outperformed the long-term averages, especially investments in top-quartile deals.”

Deal Flow Momentum

According to our data, for the first time, PE activity accounted for more M&A deals in 2021 than Corporate activity. Q1 2022 looked to be a continuation of 2021’s record deal volumes, but we saw a steep drop-off in Q2 and a month-to-month decrease in deal activity since March. Despite this recent deceleration, with 4,771 closed deals, 1H 2021 represented the second-highest closed deal activity on record for this period, with the previous period’s 5,521 deals being the highest. All told, with 2H numbers still to be written, 2022 still has potential to be a strong year for PE deal activity.

M&A pros on our recent webinar anecdotally suggested that deal flow has somewhat stabilized over recent quarters. McGowan remarked that the lower middle market stays relatively unfazed by economic factors, with deal flow at Pickwick Capital Partners remaining strong through Q4’s downswing – though he observed a recent dip in deal quality. Megan Kneipp, Managing Director of Business Development at Blue Point Capital Partners, pointed to strong deal flow and improved deal quality since the end of Q2, compared to the first half of 2022. These indications of healthy deal flow could give way to corresponding closing volumes in the quarters ahead.

Competing for Quality

Given market conditions, the plethora of business owners approaching retirement age are incentivized to sell quicker – and at deeper discounts – than perhaps planned. Moreover, with capital ready to be deployed, PE fund pockets are deep. Buy-side demand for deals coupled with a large supply of assets for sale may just mean a perfect storm for high competition to acquire quality assets.

Simultaneously, a disconnect in expectations around valuations is evident and may impact firms’ likelihood to close. In some cases, this uncertainty is being leveraged to equity investors’ favor. During July’s webinar, sell-side panelists referenced deals wherein prospective PE buyers have cited the current economic environment as well as comparable valuations for publicly traded companies to lowball bids for private companies.

Not only do business owners have a mindset to sell, but the growing willingness of firms to buy sponsor-owned portcos shows no sign of reprieve. Our data reveals over 5,100 assets acquired by PE funds between 2013 and 2018 that are still being held – and are ripe to trade again in the years ahead. Our Private Equity Harvest Report allows investors to track sponsor-owned targets within specified investment criteria – enabling them to monitor opportunities and preempt auction processes with targeted relationship development efforts.

A Time to be Strategic

All hopeful signs point to one scenario: a flight to quality for PE. Promising opportunities exist, and PE firms have ample dry powder on hand. The challenge facing investors today is to develop a thoughtful strategy to avail themselves of those opportunities.

The more focused on their target, the more likely a firm is to win deals in today’s environment. Thus, the trend toward a more sector-focused strategy is poised to continue. Deal originators with a tightly defined investment criteria are well-positioned to leverage technology like SPS, tracking deal data in over 560 sub-industries on the most granular level, to maintain a proactive deal sourcing engine by identifying and nurturing valuable relationships within focus segments.

While data alone can’t win you deals, using data analysis and automation technology can enable you to preemptively build connections to source quality deals more efficiently than the competition.