This is Part 1 of a two-part summary of key insights from Bain & Co.’s 2024 Global Private Equity Report. Part 1 focuses on the key challenges facing the private equity industry today.

The PE industry has experienced robust growth and transformation over the last decade. With a focus on operational value creation in new and emerging markets and an embrace of technological innovation, private equity firms have raised larger pools of capital than ever before and – until recent years – deployed that capital at a rapid pace, fueled by favorable market conditions and ample liquidity.

As the industry approaches a critical juncture it is confronted with various roadblocks as well as opportunities for value creation, as revealed by Bain & Company’s recent 2024 Global Private Equity Report.

Rocky Terrain

The report sheds light on the most pervasive challenges facing the industry today:

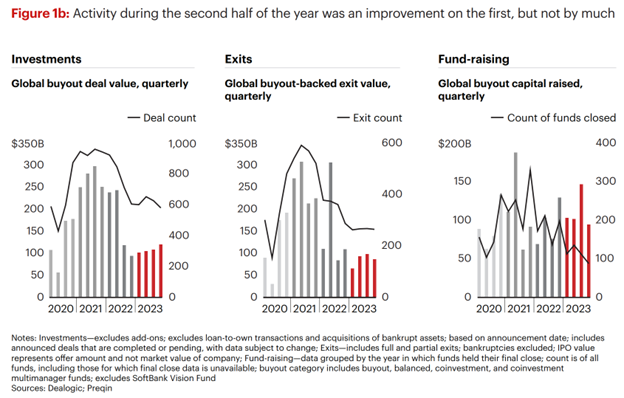

Dropoff of Deal Activity and Value: Recent trends have shown a drop in overall M&A activity since its Q4 2021 peak, as interest rates rose sharply over an 18-month period beginning in March 2022. According to SPS data, M&A deal volume in 2023 decreased by 16% from 2022. A key finding of Bain’s report also pointed to the significant decline in the deal value of the global buyout market, representing the steepest drop since the global financial crisis of 2008.

Record-High Uninvested Capital: With all-time-high levels of dry powder, over 25% is aged four years and above, presenting both opportunities and risks to investors as they seek to deploy funds effectively in a competitive market environment.

Compressed Exit Channels: PE asset exit channels, including IPOs, PE sales, and strategic sales, are all experiencing compression. This phenomenon is attributed to the high cost of capital hampering the ability to achieve desired valuations and returns.

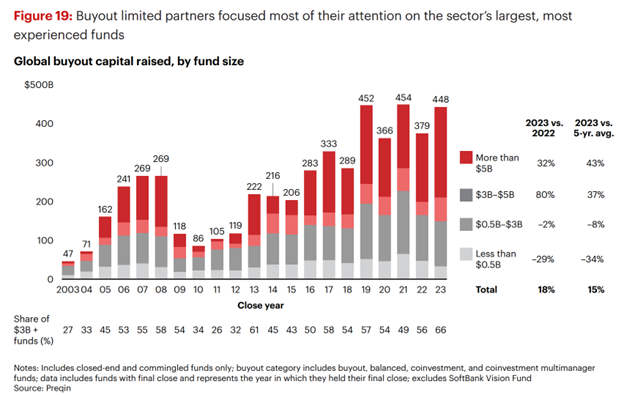

Concentration of Capital: In his analysis of the report, Hugh MacArthur, chairman of Bain & Company’s global private equity practice, highlighted the growing concentration of capital among larger funds, with 20 out of 1700 firms accounting for half of the $400 billion of buyout capital raised last year. This trend presents challenges for smaller and middle-market funds, as they compete for limited investment opportunities in an increasingly crowded market.

Value Creation Dynamics: Over the last decade, Bain’s analysis reveals that 53% of overall return in buyouts stemmed from revenue growth, while the remaining 47% was derived from multiple expansion. Notably, there was negligible contribution from margin expansion.

While complex, these challenges demand adaptability, resilience, and innovation to overcome – attitudes that are not new to private equity.

Stay tuned for Part 2 of this summary next week, which will dive into key levers for PE to mitigate current market condition and opportunities for growth in the years ahead.