After a golden age in private equity, the market has faced a transitional period over the past few years, marked by a significant downturn in deals, exits, and fundraising. Bain & Company’s recent Mid-Year Private Equity Report 2024 provides a detailed analysis of the industry’s performance and offers insights into the emerging trends as the market seeks to regain momentum.

A Delicate Dealmaking Environment and Tentative Recovery

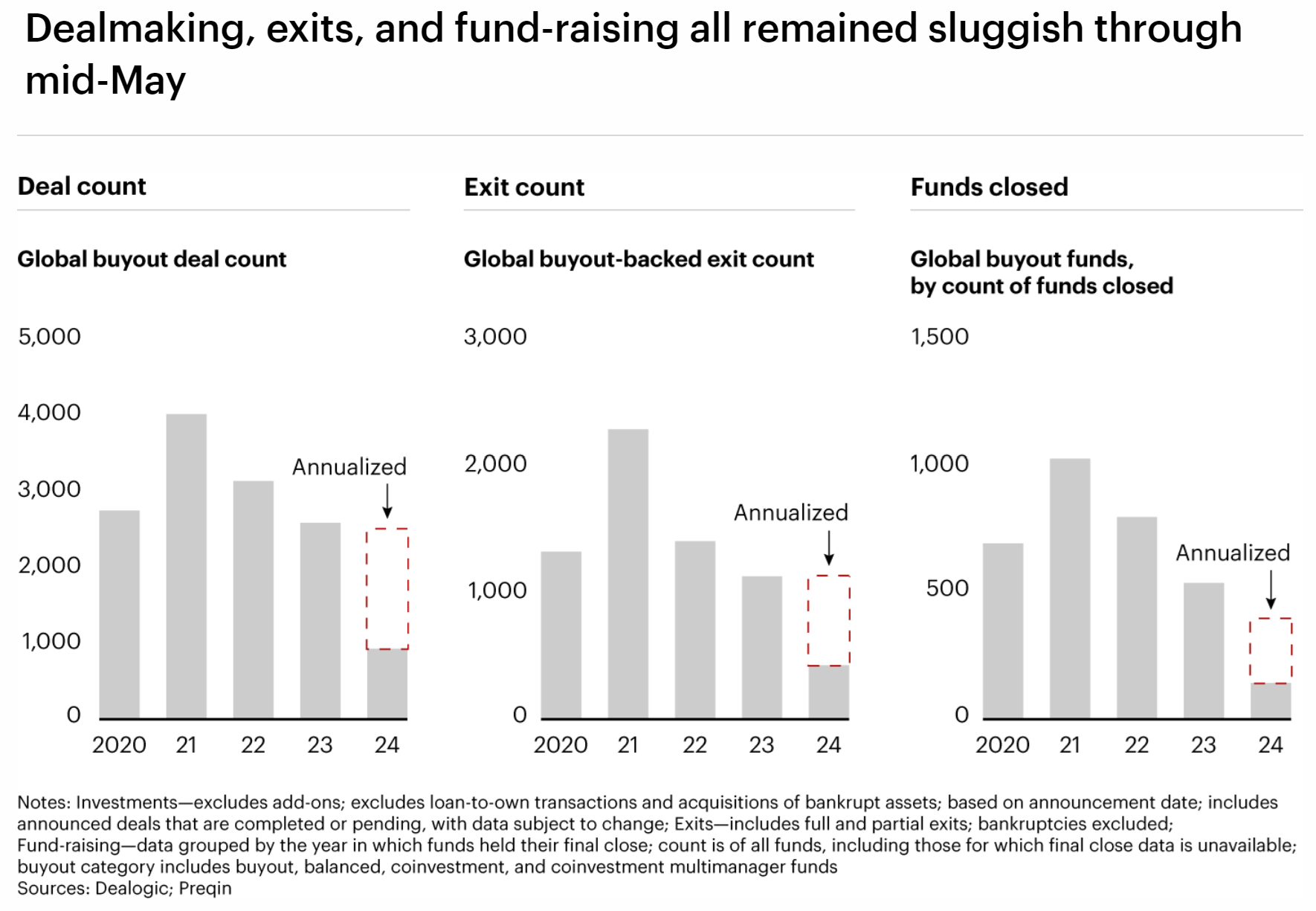

The report indicates that the PE industry’s two-year decline has begun to stabilize in the first half of 2024. Although the total deal value is projected to align with the pre-pandemic levels of 2018, the amount of dry powder available is more than 1.5 times greater than it was back then. This discrepancy highlights a market that is still finding its equilibrium after the disruptions caused by the pandemic and subsequent economic shifts.

LPs are increasingly pressing for a faster pace of distributions and are concentrating their new commitments on a select group of favored funds. This shift reflects the LPs’ desire for more immediate returns and their confidence in established funds with a proven track record.

In this context, tools like the Deal Origination Benchmark Report (DOBR) and PRISM from SPS by Bain & Co. become a critical tool for GPs. These reports measure the efficacy of firms’ coverage of their target segment against the market, providing a benchmark for deal sourcing performance to communicate to LPs and to guide strategic decisions.

When surveyed, approximately 30% of market participants did not expect dealmaking activity to pick up until the fourth quarter of 2024, while nearly 40% believed it would take until 2025 or beyond.

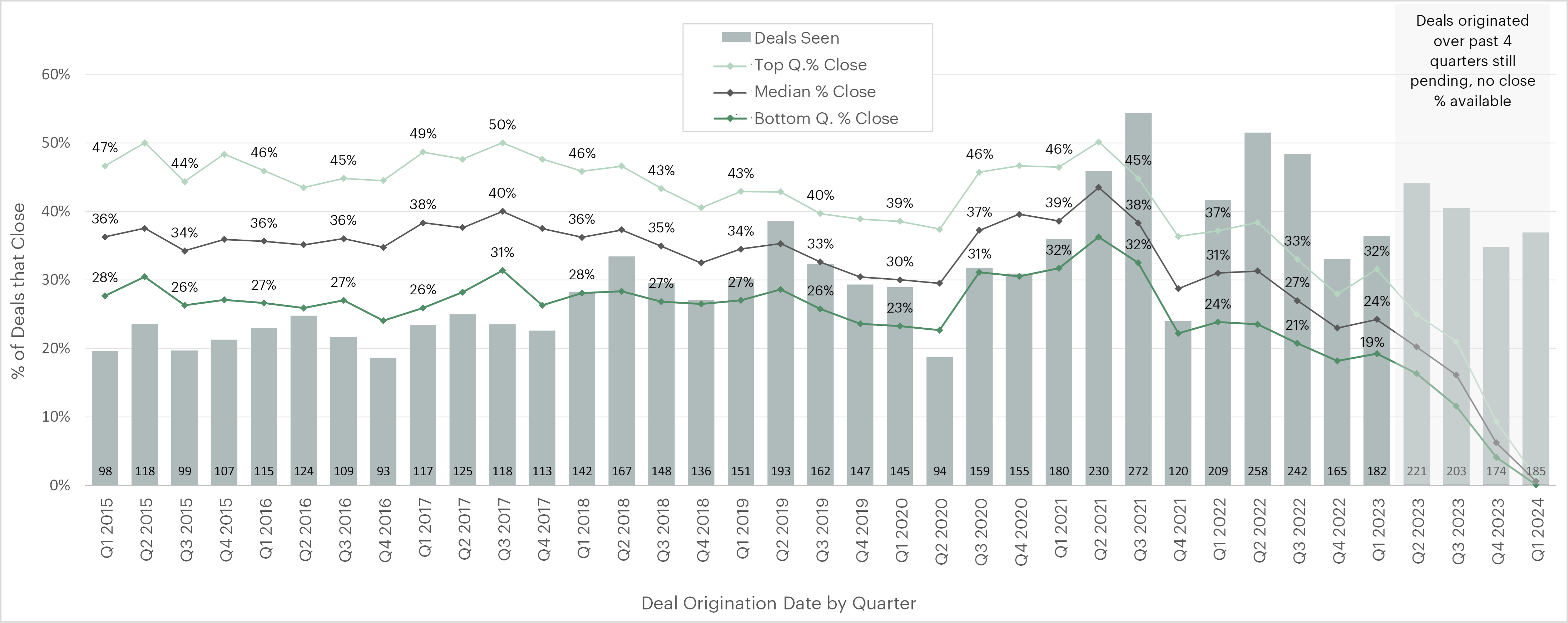

However, informal discussions with GPs indicate that deal pipelines are refilling, and there are early signs of a recovery taking shape. According to SPS’ latest Science of Deal Sourcing analysis, aggregate PE pipeline data reveals that Q1 2024 median deal flow had increased from the previous period and also surpassed pre-pandemic levels, which may suggest a market getting back on track.

Continued Liquidity Struggles

Fundraising remains a challenge for most funds, as they struggle to attract fresh capital in a market still recovering from the effects of the pandemic and economic uncertainty. Bain’s report suggests that GPs who are unable to guide their portfolio companies to successful outcomes may face a market shakeout.

The current environment also poses a significant liquidity challenge for PE firms. Many are grappling with exit overhang, and a considerable number are closing below target. With five-plus years becoming the norm for holding periods, firms need to carefully assess the health of their portfolio. SPS allows firms to compare their portfolio holdings to other assets that are being held or sold within their target segment, information that is vital for GPs to make decisions about whether to hold portfolio companies longer or source more add-ons to enhance portfolio value before exiting.

And for PE firms looking to exit their investments in the near term, selecting the right sell-side intermediaries is crucial. GPs can utilize SPS to evaluate intermediaries based on their track record over the last three to five years, ensuring that firms align with partners who can effectively navigate the complexities of the current market and maximize exit values.

Strategic Moves for GPs

The report outlines practical ways for GPs to stimulate activity and generate returns. These include focusing on innovation to address cash challenges at buyout-backed companies and rethinking exit strategies to adapt to the changing market conditions.

The secondary market is gaining prominence as a potential solution for the industry’s liquidity needs. According to Bain’s report, expanding this market could provide the necessary impetus for PE firms to navigate the current landscape more effectively.

The SPS Private Equity Harvest offers a solution to navigate the current exit environment. A comprehensive view of active portfolio companies with longer-than-average holding periods reveals ample opportunities to source from other sponsors.

Generative AI is also recognized for its transformative potential within the PE sector. Investors are leveraging these technologies to enhance decision-making, transform companies, and improve returns. GPs must remain vigilant and proactive in experimenting with new tools to identify opportunities and navigate the market’s complexities.

Looking Ahead

While the PE industry has historically shown resilience in the face of adversity, the path to recovery will require strategic innovation and adaptability. GPs must be proactive in exploring new avenues for growth and returns, while LPs will continue to play a crucial role in shaping the industry’s future.

Staying equipped with expert insights and technological tools will be essential for GPs to understand the trends and prepare for the future of private equity investment. As the industry moves towards a recovery, these resources will be crucial in guiding strategic decisions and fostering growth in a delicate environment.