This blogpost is a summary of SPS data points referenced in Bain & Company’s Global Private Equity Report. Download the full report here.

The hard facts of 2022’s deal activity – namely a first half high following a record-breaking 2021, and a steep H2 decline due to interest rate hikes and persistent inflation – are viewed by some as objective functions of the market, like the law of gravity: what goes up must come down.

But further inspection may reveal the slowdown in deal-making is more accurately explained by reflexivity – attributing market activity to the influence of investors’ perception of the environment, rather than the environment itself. Throw in mixed signals from the Fed and a speculative climate, and you might have a recipe for the current moratorium in PE deal-making.

Whatever your lens to examine the current environment, the laws of M&A dictate that eventually, the waters will calm and deals will be done again. And when they do, investors would do well to stay aware of the trends controlling the tides.

Bain & Company’s Global Private Equity Report, released annually in Q1, dissects the anatomy of the current slowdown, characterized by a lack of clarity with regard to the path ahead and investors’ ensuing apprehension to transact. The report then examines the trends projected to command deal activity in the quarters to come.

Below are some highlights applying SPS data:

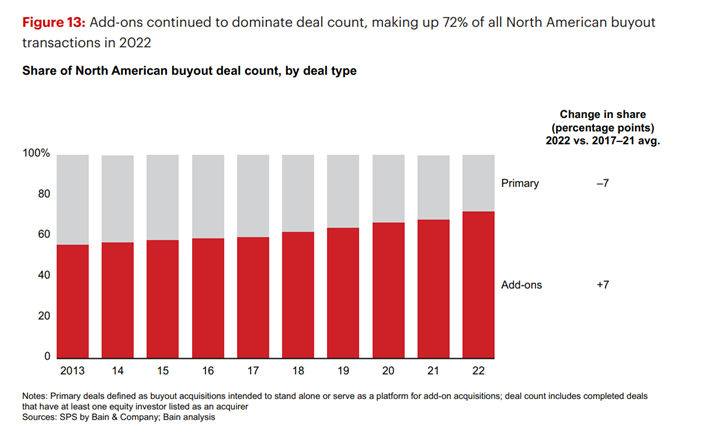

- Buy-and-build and rollup strategies remain attractive to sponsors with the number of add-on deals rising as a proportion of total deal count. Emerging in the 1980s as somewhat of a novelty, consolidation strategies involve acquiring smaller companies and combining them into larger ones with higher valuations. Today, the tactic is a major part of the playbook for most private equity firms, picking up steam over recent decades and even accelerating further in 2022 against a grim economic backdrop. According to the report, add-ons made up 72% of all North American buyouts in 2022 by deal count. And by SPS, by Bain & Co.’s record, 2022 saw 2.6 add-on transactions for every primary platform acquisition. The sustainability of consolidation plays through recent economic confusion is likely attributable to sponsors’ inclination to stick to smaller, more feasible deals while pausing on larger transactions until market direction is ascertained.

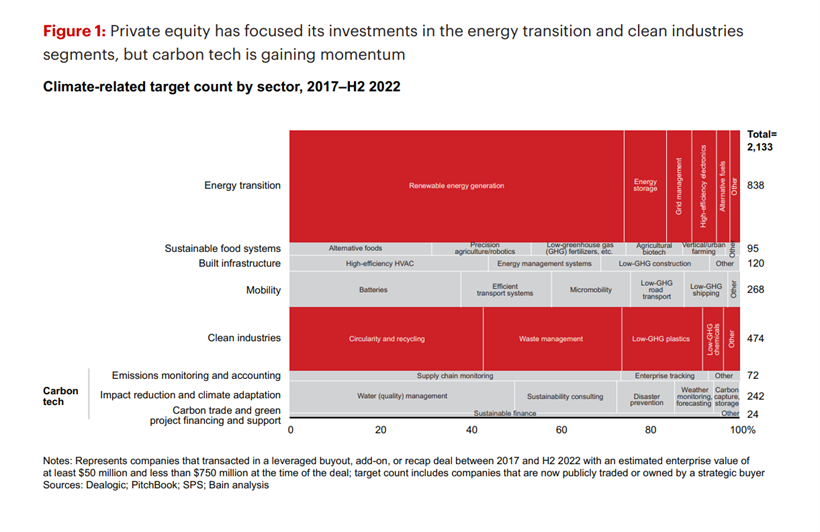

- Investors are also tasked to look beyond today’s landscape to the forces that will shape the future of the global economy – with a major focal point being the transition toward clean energy. With the call to shift away from carbon-based fuels amplifying on a macro level, funds are simultaneously faced with the risk decarbonization poses to their current portfolios, as well as the opportunities to capitalize on the ample green space it creates. According to SPS analysis cited in Bain’s Global PE Report 2023, firms have been focusing deployment within the Energy Transition and Clean Industries segments, while Carbon Tech sectors are not far behind. The report indicates that, “between 2017 and the first half of 2022, buyout and growth equity funds had done energy transition–related deals with a total reported value of around $160 billion, the majority of it concentrated in the renewables and clean industries segments.”

As interpretations of economic conditions are in flux, M&A investors are turning to trends like these to refine their investment strategy and be prepared when the tides inevitably turn, and dry powder is ready to be deployed.

By leveraging data analysis technology like that offered by SPS by Bain & Co., firms can get a comprehensive view of the most attractive segments to invest in relative to their investment criteria, and even drill down to the individual advisors actively closing add-on transactions in their target market. Find out how SPS can fit into your origination strategy today.

See Bain & Company‘s full Global Private Equity Report 2023.

Watch Bain & Co.’s webinar diving into key insights from the report, featuring high MacArthur, chairman of Bain’s Global Private Equity practice.