SPS recently published the 2023 Deal Origination Benchmark Report, finding that PE firms had an average 17.8% Market Coverage – or the share of relevant closed deals logged in PE firms’ pipelines – during the 2023 period. This year’s average Market Coverage has fallen slightly from the 2022 edition of the report but remains consistent with recent years.

The report, released annually each fall, uses last-twelve-months (LTM) data for the year ending June 30, 2023. It provides detailed analysis on sponsors’ deal sourcing strategies relative to peers, allowing firms to gauge the efficacy of their origination efforts and identify tactical areas for improvement in the year ahead.

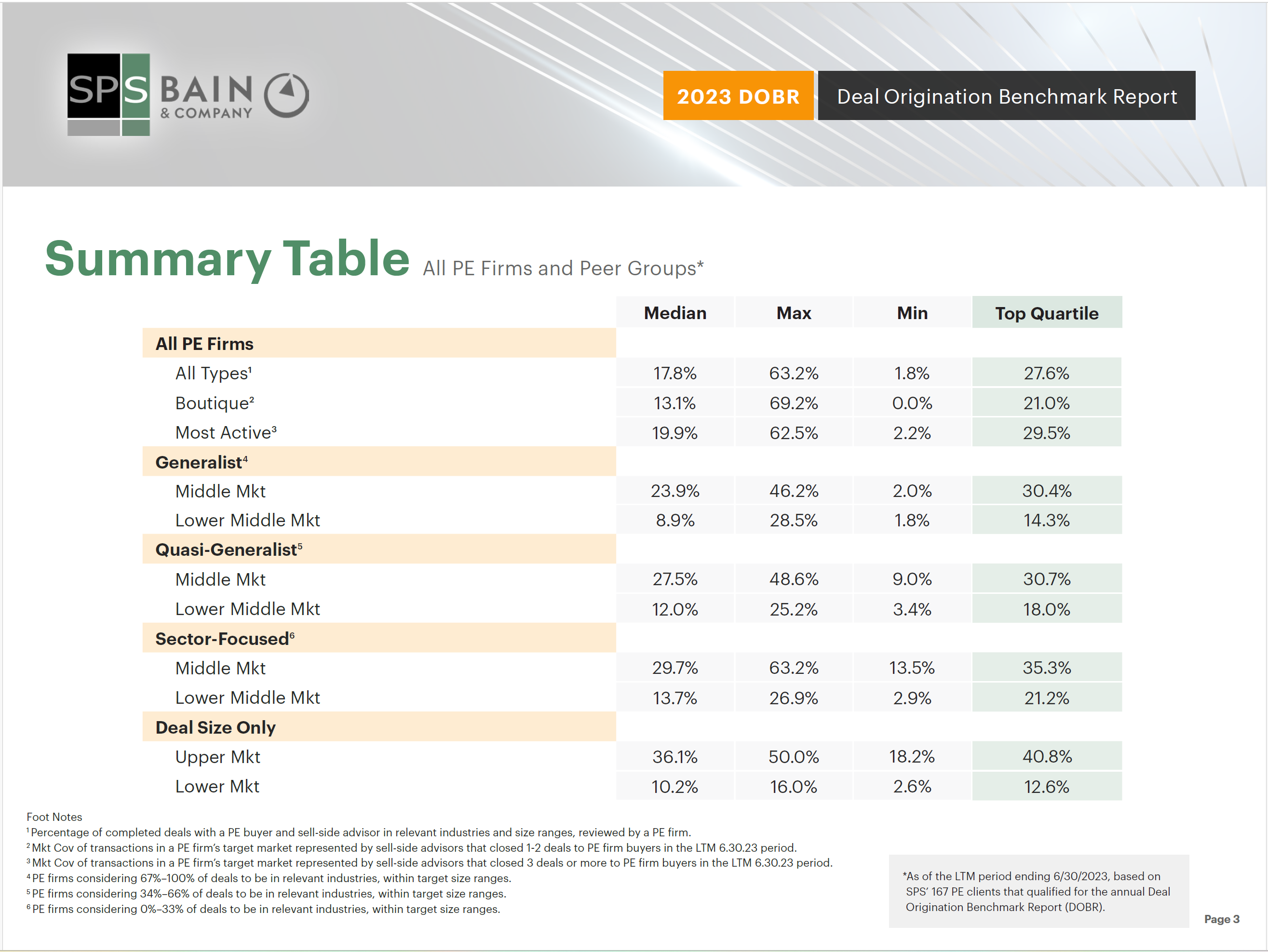

Each SPS client receives a custom DOBR comparing its Market Coverage to the overall industry and a peer group of similar private equity firms, defined by target investment criteria. The 2023 edition includes results from 167 qualified PE firms segmented into 8 different peer groups.

While target market coverage has remained relatively low for the overall industry, some private equity peer groups saw a much broader portion of relevant deals. Upper Market-focused funds see a median 36.1% of deals in their target market. Middle Market-focused firms across Generalist, Quasi-generalist, and Sector-focused peer groups typically see over 24% Market Coverage.

Conversely, Lower Market-focused firms saw only a 10.2% share of target market deals during this period, while Lower Middle Market-focused firms in Generalist, Quasi-generalist, and Sector-focused peer groups had Market Coverage metrics of 8.9%, 12.0%, and 13.7%, respectively. One underlying reason for a greater Market Coverage percentage among firms focused on larger deals may be a trend toward broader auction processes for deals in higher size ranges.

Though Market Coverage for most peer groups has decreased or remained relatively consistent year-over-year, firms in the Upper Market, Lower Market, and Generalist, Middle Market peer groups have seen an increase from 2022, which may suggest improved deal sourcing practices among firms in these groups.

Steady Market Coverage for the PE industry is set against a backdrop of tapering deal flow, which has declined by 6.9% across all PE peer groups. Some peer groups saw much steeper declines, with median annual deal flow for Generalist, Lower Middle Market and Sector Focused, Lower Middle Market firms falling by 19.0% and 27.4%, respectively. During the same period, the median Pipeline Closing percentage – or percentage of deals logged that ended up closing – dropped by 5%.

Relatively flat coverage of relevant deals amid dwindling deal activity suggests weakening quality of deals coming to market for most PE firms. To combat this, many funds are further emphasizing deal origination as a core practice, focusing on expanding their intermediary reach and ensuring maximum coverage.

See more key findings from the recent 2023 Deal Origination Benchmark Report, or request a demo of the SPS platform.