As the demand for climate accountability and the global call for decarbonization amplify, capital has flowed rapidly to the renewable energy sector during the first three quarters of 2021. Investment is pouring into a growing volume of renewable energy assets related to the production of or infrastructure for solar, wind and hydrogen power as well as environmental remediation methods such as carbon capture.

And where capital flows, M&A deal activity promptly follows.

The influx of private equity interest in the sector comes in response to a confluence of factors related to global politics, capital availability and economic recovery from the pandemic as well as a growing popularity of environmental, social and governance (ESG) activism.

Particularly in the United States, investment into the sustainable energy space is coming into sharper focus after years of financing ebbs and flows. A core tenet of the new administration’s pledge to stimulate job growth and clinch the US’ status as the vanguard in clean energy technology, the government’s current outline to reach net zero carbon emissions by 2050 would require between $1 trillion and $2 trillion of investment each year, according to the Energy Transitions Commission.

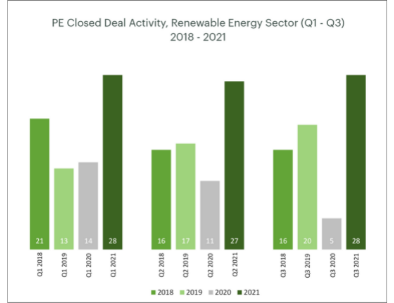

According to SPS data, there have been a total of 328 closed M&A deals in the energy sector already in 2021, with 25% of these falling under the renewable energy umbrella – primarily including production, service, and equipment companies. This reveals a 10% increase in closed deal volume for the renewables sector in H1 2021 compared to the same period in 2020, and a 13% increase from pre-pandemic levels in H2 2019. Of deals closed in the first three quarters of 2021, renewable energy producers and service companies are the frontrunners, accounting for 39% and 35% of total deal volume, respectively.

The chart below demonstrates monthly closed deal activity for the first three quarters of 2021 compared with the same period since 2018.

Yet, it’s not all good news for the energy space. The pouring of investment into renewables is cutting off the capital supply to long-favored conventional assets like coal, oil, and gas. In fact, for the first time, banks are on track in 2021 to commit more financing to sustainable projects than to these traditional energy assets, Bloomberg reported in May.

The table below, generated from SPS data, demonstrates the most active intermediaries in the renewables game over the last 3 years.

Moreover, private equity investment growth in green energy production, services, and infrastructure is fast surpassing fundraising for traditional assets, with private equity funds that are dedicated to renewable energy assets outpacing fossil fuel funds by a multiple of roughly 25, according to Bloomberg. Data generated from SPS mirrors this trend, showing a 13% decrease in PE deal activity for these traditional sectors in H1 2021 compared to pre-pandemic H2 2019.

An intensified call for climate accountability and the global target for net zero carbon emissions mean that demand for renewable energy resources and utilities is expected to continue to strengthen in 2022, signaling for higher volumes of new commercial projects and technologies in the sector. These new investment opportunities, paired with rebounded capital supply from the fallout of the Covid-19 pandemic, point to strong M&A deal activity in the quarters to come.

Chart and table generated from SPS proprietary data