Renewables and the clean energy transition have emerged as prime investment avenues for private equity investors, marking a significant upward trajectory over the past decade and with expectations for continued growth in the years ahead. As Hugh MacArthur, chairman of the private equity practice at Bain & Co. indicated, “We are already seeing a substantial increase in things like energy transition… an area that a lot of investors are going to pile into as an attractive space.”

With global commitments towards sustainability, the escalating demand for clean energy solutions not only aligns with environmental imperatives but also promises substantial returns for investors in a dynamically evolving market. Industry executives across oil and gas, utilities, chemicals, mining, and agribusiness are increasingly recognizing the potential of regions like North America, with 79% of professionals surveyed viewing it as “an attractive hub for energy transition investments”, according to a Bain brief.

Supported by an SPS deal activity analysis into the clean energy transition market, it’s evident that the space represents a burgeoning investment landscape. To capture the full extent of the growth occurring in this nascent market, this evaluation includes transactions involving climate technology, infrastructure, and services companies that are supporting the energy transition, as well as traditional renewables.

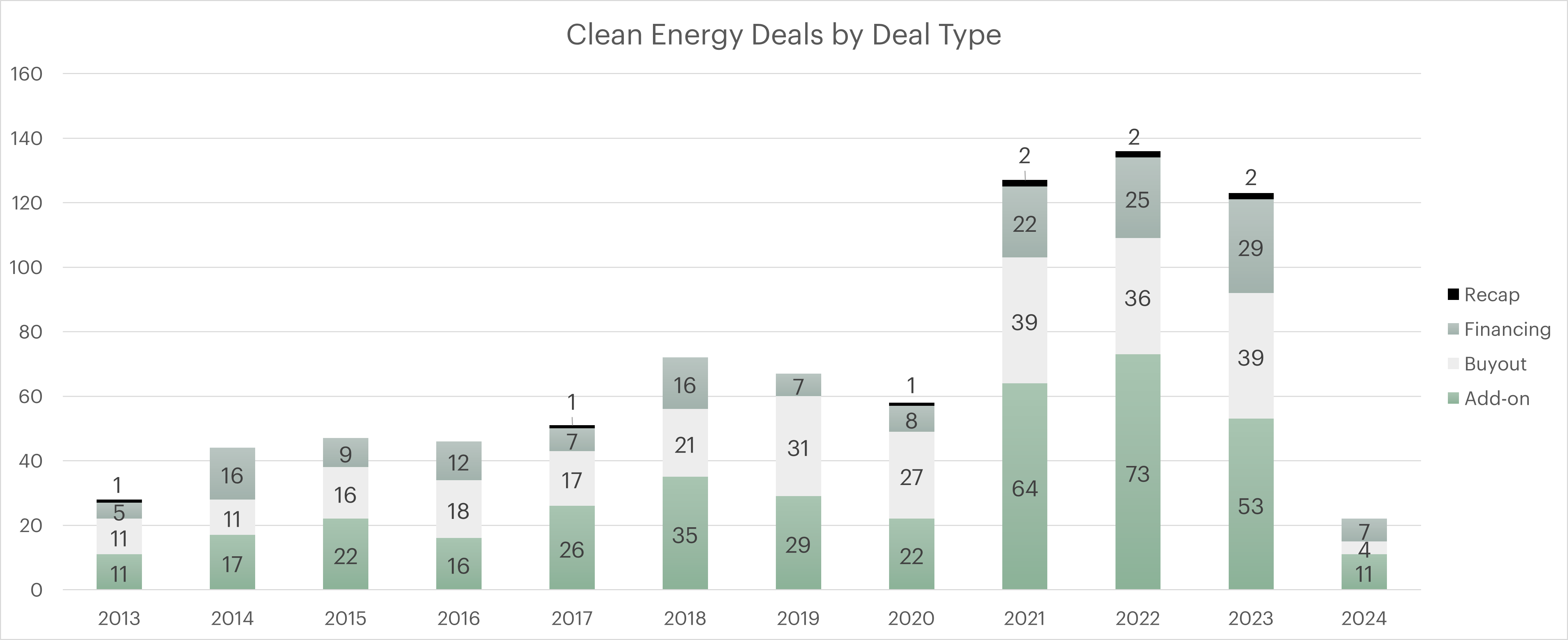

Following the COVID-19 pandemic, the clean energy segment experienced a remarkable 124.5% surge in transactions from 2020 to 2021, with a continued 4.2% year-over-year increase extending into 2022. Despite experiencing a slight downtick amidst economic uncertainties in 2023, deal activity in this segment declined to a lesser degree compared to some other sectors, and weighed in at a 66.6% increase from pre-pandemic levels in 2019. While the first quarter of 2024 saw a slower start, the trajectory remains primed for potential acceleration.

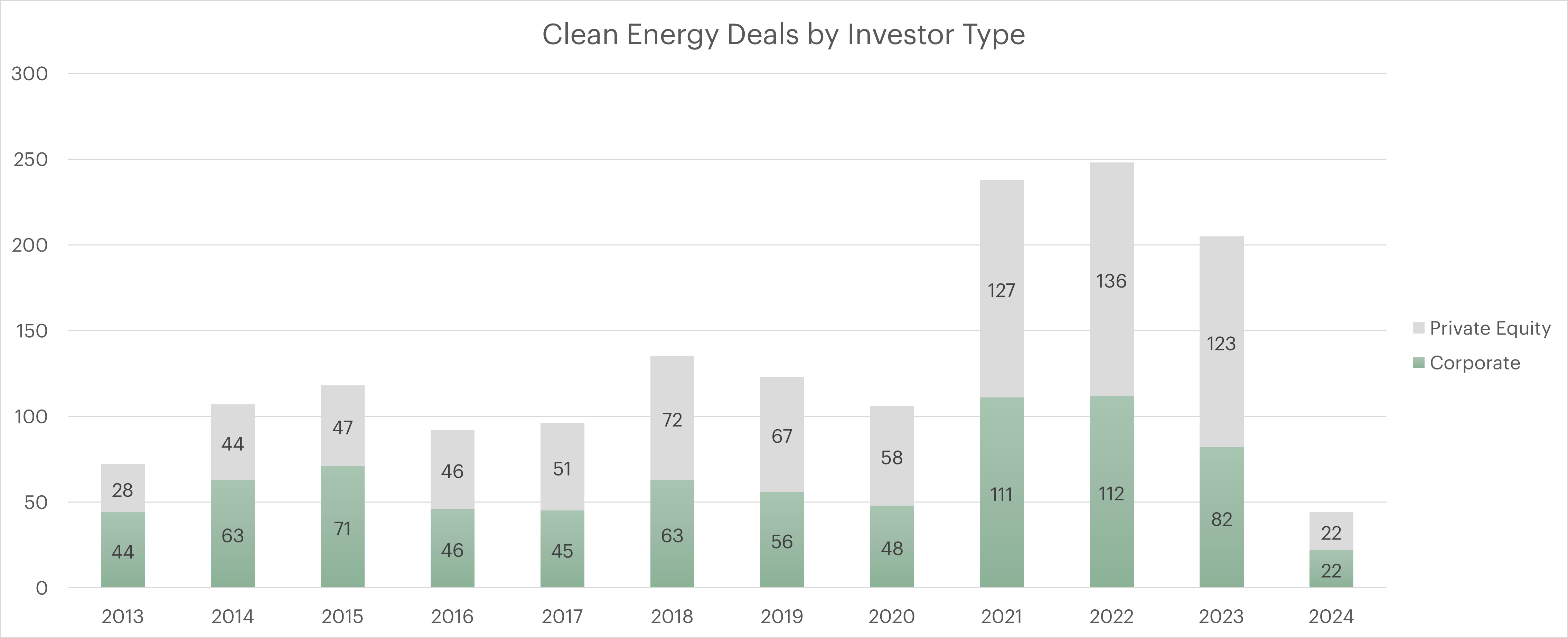

While corporate investors dominated in clean energy deal activity from 2013-2015, private equity buyers surpassed corporates in 2017 and have continued to outpace them, with PE’s share accounting for 60% of deals in 2023.

In terms of deal types, the bulk of private equity deal activity in this segment is comprised of add-on acquisitions and platform buyouts, as buy-and-build and roll-up strategies have gained popularity over the last five years or so. Despite the fall in overall deal activity from 2022 to 2023, as a percentage of total deal volume, buyouts increased during this period from 26.5% to 31.7%, respectively. This indicates a potential increase in confidence and strategic focus in this area from investors.

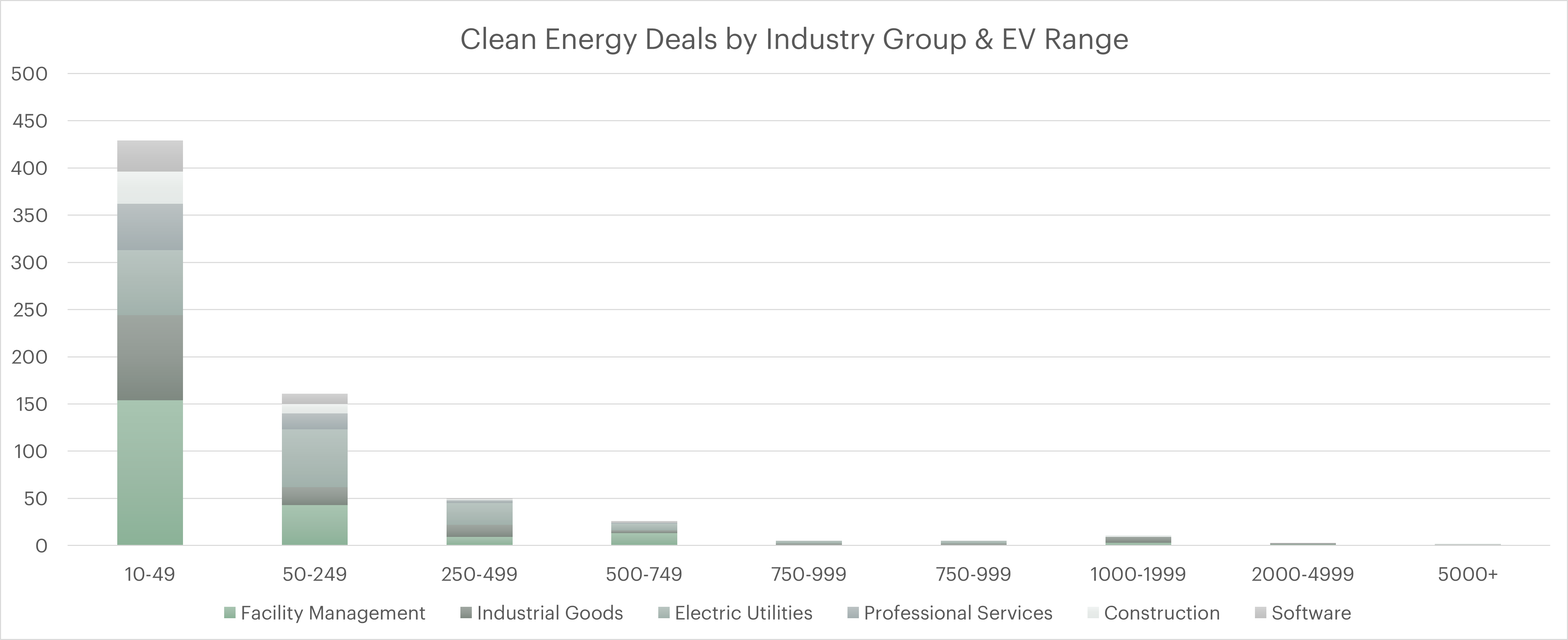

The majority of clean energy deals fall within the Facility Management, Industrial Goods, and Electric Utilities industry groups. There is a concentration of lower-middle-market transactions ranging between $10-49MM in enterprise value (EV), which aligns with an overwhelming share of add-on deals, and a lesser – but not insignificant – volume of deals within the $50-249MM and $250-499MM EV ranges.

The surge in M&A investments in clean energy underscores a fundamental shift towards sustainable and resilient energy solutions. Despite economic fluctuations, the sector continues to attract significant attention and capital, driven by the imperative to address climate change and capitalize on burgeoning market opportunities.

Ever the trailblazers, private equity investors have often been first movers in emerging markets, leveraging their capital and operational expertise to unlock value in dynamic and evolving economies. We expect their role in the global clean energy transition to be no different.