When the predecessor to Chicago-based GTCR began buying up small companies in the 1980s and combining them into larger ones, the strategy was seen as something of a novelty.

The titans of that decade, including KKR & Co, went after big fish and swallowed them whole. Who needed to do add-on deals when you could generate sweet returns from leverage alone?

Forty years later, you’d be hard-pressed to find a private equity firm, including KKR, that doesn’t sponsor consolidation plays.

“The buy-and-build has become one of the foundational playbooks of private equity value creation,” said David Harvey, president of Harvey & Co, a Newport Beach, California-based buy-side investment bank.

With 85 percent to 90 percent of its business coming from sponsors pursuing consolidation strategies, Harvey & Co closed twice as many transactions last year, just over 140, as it did in 2020, itself a record year for the firm.

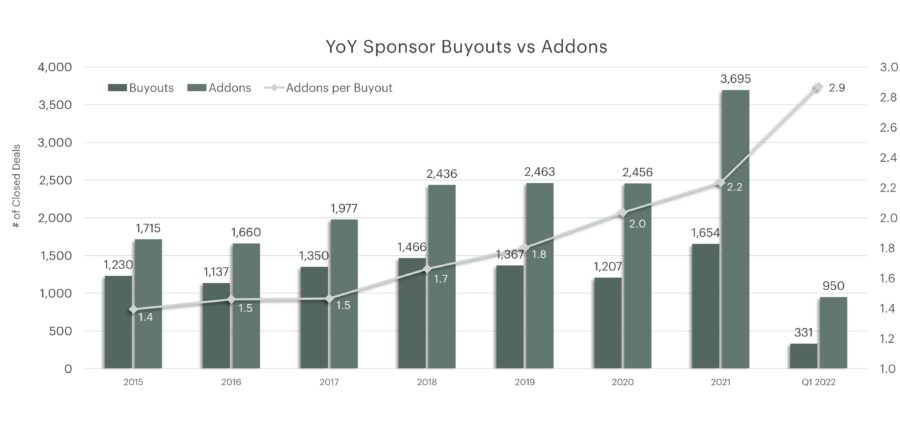

Indeed, a recent analysis of North American deals by sourcing platform provider SPS by Bain & Co found that sponsors made 2.9 add-on acquisitions for every platform acquisition in the first quarter of 2022, or 950 add-ons to 331 platforms. That ratio has grown over the last seven years, up from just 1.4 in 2015, to 1.7 in 2018, to 2.2 last year.

Along with GTCR and its spin-offs, including Thoma Bravo, firms well-known for their consolidation strategies include Boston-based Audax Group (126 add-ons since the beginning of 2020, according to SPS by Bain & Co), Cleveland and New York City-based The Riverside Company (62) Chicago-based Madison Dearborn Partners (58), New Mountain Capital (55).

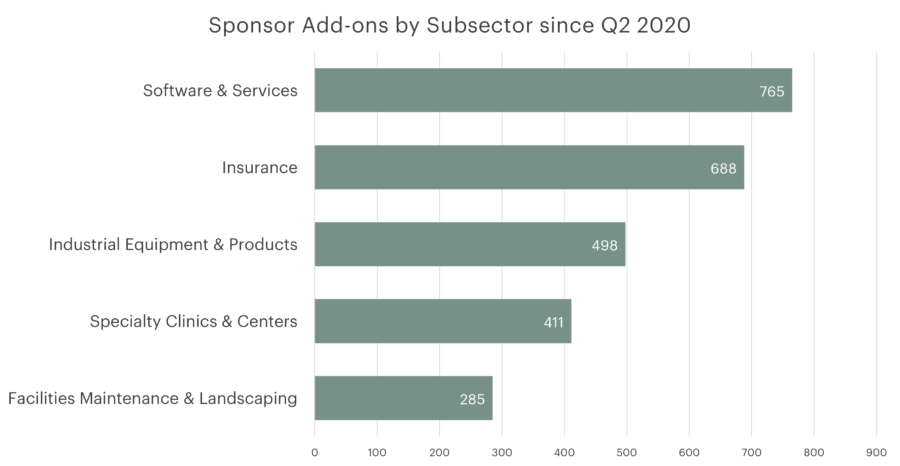

Sub-sectors that have seen vast amounts of sponsor-backed consolidation over the last two years include software and services, insurance, industrial equipment and products, specialty clinics and centers, and facilities maintenance and landscaping.

Any kind of regional business, whether residential or commercial, lends itself to consolidations, said Harvey, pointing to residential HVAC services and fire and safety businesses as examples. Local businesses can be combined into regional businesses; those can be combined into super-regional businesses; and those can be combined into nationwide businesses.

A number of developments in the market have combined forces to power the consolidation trend. That’s according to Harvey and to fellow investment banker David Deutsch, president of David N. Deutsch & Company. Deutsch’s Bedford, New York firms specializes in structured, negotiated company sales, in addition to providing board advisory work and hosting what Deutsch describes as a “long-standing client/CEO investment group and legendary conference in Saratoga Springs.” Among the most prominent of those forces:

- The growth in “practiced acquirers”: Over the past 10 years or so private equity firms have staffed up to become what Deutsch calls “practiced acquirers.” Many employ teams of people devoted just to originating add-on transactions; their work in some cases is supplemented by that of buy-side investment banks. Often sponsors employ teams of operations specialists who make sure the integrations go smoothly. It all adds up to an efficient ecosystem geared toward add-on deals.

- The Arbitrage: “Simply put, they’re highly accretive,” said Harvey of add-on deals. Sponsors, he said, can pay seven or eight times EBITDA on average for a series of small companies and then sell the beefed-up platform company for up to 12 to 15 times. “The typical arbitrage is three to four times the EBITDA that they’re buying, if not more,” Harvey added. “With that kind of arbitrage available, sponsors want to do as much of that as they can.”