Each year, we publish an outlook on private equity deals in the quarters ahead through the lens of a proprietary analysis of historical activity – unique to SPS data alone.

The headlines on PE and M&A deal activity have been bleak over the past year or so. With a confluence of macroeconomic conditions creating a perfect storm for a slowdown, and the reinforcing effect of market sentiment driving hesitation to buy and sell, firms are questioning what it will take for deal activity to revitalize.

By nature, financial market behavior relies on a dynamic relationship among the factors influencing it. And any professional who’s been around the block knows, in terms of a bounce-back, it’s not a question of if – but when. In searching for the answer, firms may turn to their own deal pipelines or anecdotal signs of life to capture an outlook.

SPS’ ninth edition of The Science of Deal Sourcing 101 offers a more data-driven approach. After twelve years tracking the behavior of deal activity through fluctuating market conditions and unprecedented global events, we’ve cultivated an objective analysis to observe and predict deal volume in the M&A market within historical context.

To set the stage, deal activity declined by just under 15% in 2022 compared to the previous period, and is on track for a similar decline in 2023. For the first time ever in 2021, PE activity represented the majority of M&A activity compared to strategic buyers, and this trend has continued ever since – with PE activity consistently representing 53% of overall deal activity since 2021.

On a quarterly level, deal volume climbed from a low point in Q2 2020 to a peak in Q4 2021, only to decline in each consecutive quarter since. Q1 2023 activity was down 25% from the same period in 2022, and by our counts so far, Q2 2023 activity was down by a similar amount compared to Q2 2022 (Note: The percentage change for Q2 2023 will decrease as more closed deal data is collected).

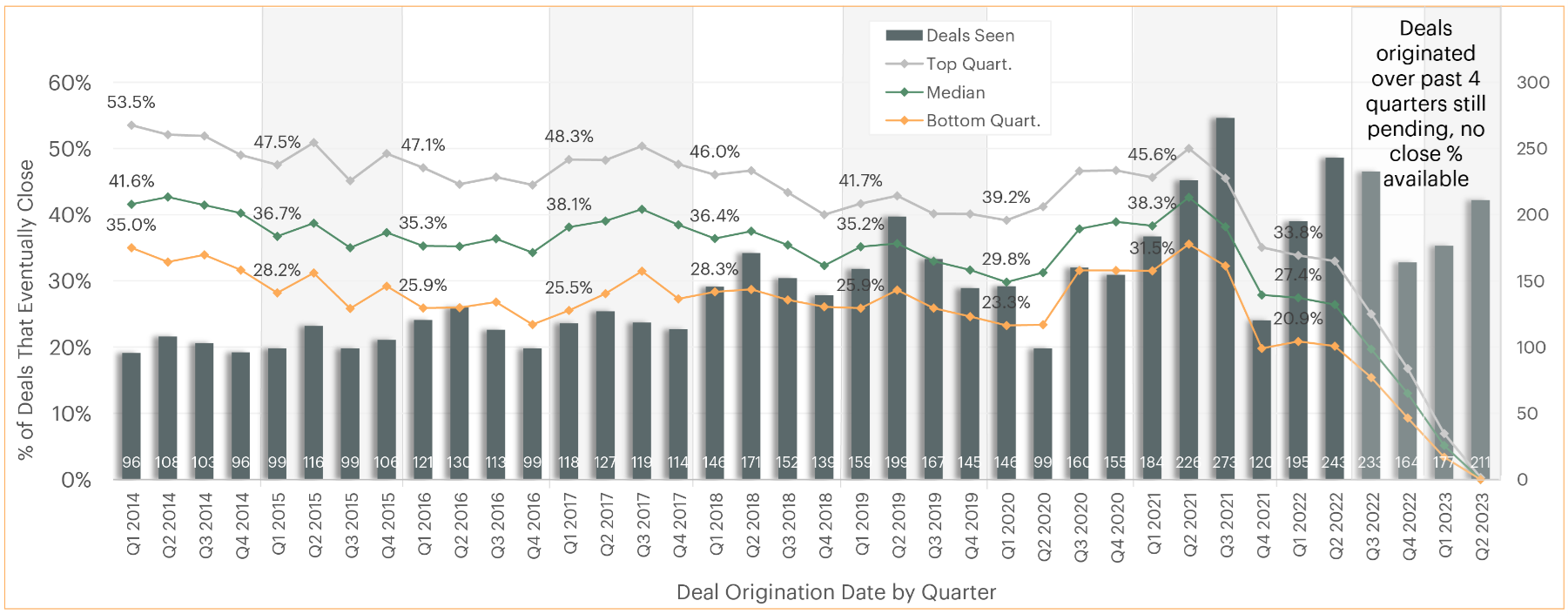

Median Deals Originated vs. % Closed – by Quarter

Unique to SPS data, the chart above compares quarterly PE median deal flow (columns) to the percentage of those deals launched that eventually close (lines). Based on historical averages, PE firms typically close deals approximately 7 months after sourcing, and only 30-40% of deals that PE firms log end up closing.

As the COVID-19 pandemic ramped up, a lower-than-typical share of deals that launched between Q4 2019 and Q1 2020 ended up trading. The portion of deals that would end up closing then sharply bounced back for deals brought to market in subsequent quarters, peaking in Q2 2021. The percentage then dipped heading into 2022, and has remained lower than the historical median ever since (Note: Percentages for the most recent quarters may be restated at higher levels when this analysis is updated next year.)

All said, the sense of global uncertainty of recent years is surely represented in this year’s analysis, with a stark deviation from historical patterns. One such shift is evident in the comparison between deal flow and closed deal volume since 2021; historical patterns would suggest high closed deal volumes whenever deal flow is robust. Yet, even with Q2 2022 deal flow being the highest on record for this period, the percentage of deals launched during this period that ended up trading was below 30%, suggesting a mismatch between deal quantity and quality.

Of course, there are other factors at play that may be affecting deal logs and the likelihood or time to close. It is possible that given the current economic environment, deals are simply taking longer to close. There’s also a case to be made for firms’ adoption of better deal sourcing tactics, leading to higher competition for deals and those deals showing up in more firms’ pipelines.

There is also a higher likelihood of stalled or broken processes during the period of tightening rates and rising inflation over the past year. SPS’ Pipeline Analysis and Broken Deal Alerts features enable PE firms to monitor the trading status of relevant assets they’ve identified – as well as the individual intermediaries involved with them – to move swiftly when opportunities resurface.

At the same time, intermediary churn has been higher over recent years than ever, making traditional methods of deal sourcing even more difficult. PE firms can combat high churn rates with SPS’ CRM Integration tool to automatically update CRM data to eliminate staleness, streamline outreach, and maintain a robust deal-sourcing operation.

Despite a slow year so far, some industry experts are pointing to signs of life, with panelists on our recent PE webinar expressing optimism for deal activity to pick up in the second half of the year. Whether this outlook holds true or not, an eventual comeback is inevitable – and PE firms can prepare by using technology and automation tools to capture quality deals and beat out the competition.