A year ago, families, communities, and nations were grappling with how to deal with Covid and coming to terms with its longer-than-expected impact, filling us with uncertainty and dread for what it could mean for our health, finances, and loved ones. Fast-forward to today. After a challenging and, for some, devastating year dealing with the pandemic, it seems we’re ready to share a collective sigh of relief in Covid’s aftermath. But did we skip going back to “normal” and instead go straight to “crazy”?

If you’ve been to the airport or traveled by road recently, you probably noticed record traffic and crowds all around. This trend looks to continue as the travel and hospitality industries experience record bookings and voice concerns about being understaffed to meet consumer demand.

The private equity (PE) and M&A deal markets have also bounced back furiously from their initial sharp decline in the second quarter of 2020, showing tremendous resilience in the face of an unprecedented global pandemic. According to data collected by Sutton Place Strategies (SPS), a Bain & Co. company, PE activity was down a mere 8% in 2020 in the US and Canada compared to 2019 levels. What may come as even more of a shock is that PE deal activity was up over 55% in the first half of 2021 compared to the first half of 2020. Furthermore, as another strong sign of investor demand, purchase multiples have not contracted. According to Bain’s Global Private Equity Report 2021, deal multiples in the US were at or near all-time highs in 2020 despite the pandemic, with more than two-thirds of all deals in the US trading at more than 11 times earnings before interest, taxes, depreciation, and amortization.

In addition to the pent-up supply of deals created by Covid, there are several other factors leading to the current flurry of transaction activity. According to Bain’s report, while global fundraising was slightly lower in 2020 from its 2019 peak, it was still the third highest year on record, and including SPACs, it was the second highest. Also, potential tax changes threatening to replace lower long-term capital gain rates with higher ordinary income percentages are compelling sellers and buyers to act now rather than wait.

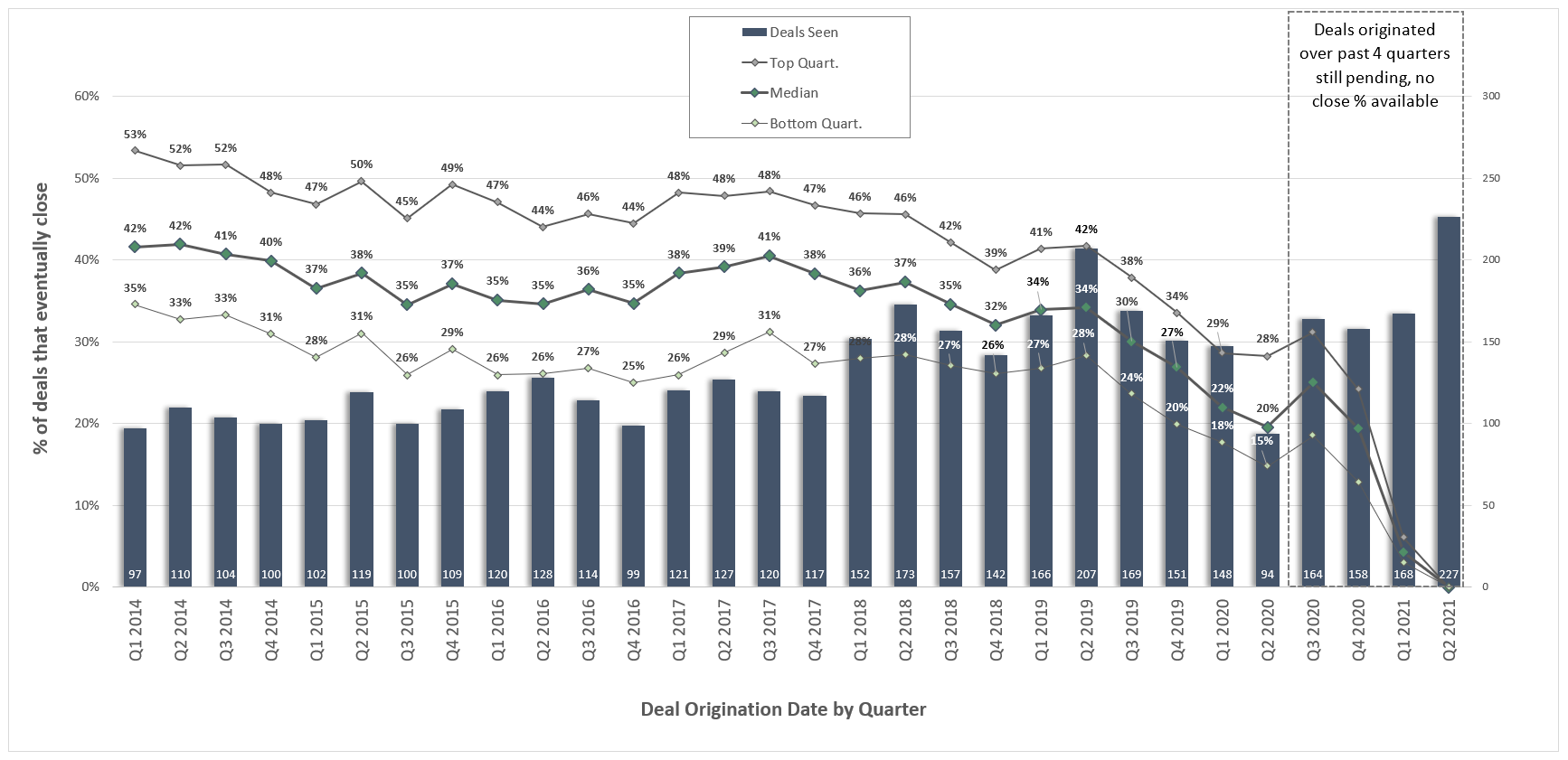

PE Deals Seen vs. Percentage Closed

As a result of Covid’s initial outbreak, PE median deal flow (the bars in the chart above) dropped to its lowest level in the second quarter of 2020 compared to the prior second quarters, which comes as no surprise. However, it rebounded sharply in the third quarter of 2020, which was slightly less than the prior third quarter, and the fourth quarter of 2020 and the first quarter of 2021 were the highest fourth and first quarters, respectively, since we started tracking the data. These trends point to increased closed deal volumes in the quarters ahead.

This is Part 1 of a two-part series on investor demand insights from H1 2021. Read Part 2 here.

Download the slides from our recent webinar for a full-scope look at PE and M&A deal origination in Q1 2021.

Photo courtesy of Unsplash

Chart generated from SPS proprietary data