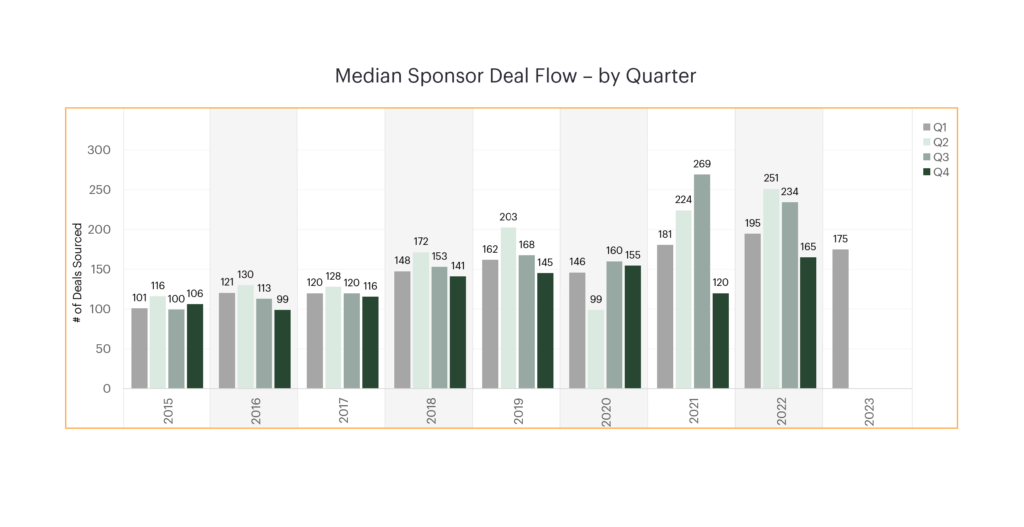

The State of PE Deal Flow – Quality over Quantity

Nearly halfway through 2023, the reality of the slowdown has begun to sink in, and M&A folks are attempting to foretell closing volumes for the remainder of the year and beyond. For any given firm, the greatest signal to the number of deals likely to close in the quarters ahead lies within their pipeline data for deals logged over preceding quarters. But with the effect of the downturn varying by sector of focus, predictions for the overall PE market are difficult to capture.

Private credit market remains open for business

The war in Ukraine, the stock market plunge, the spike in inflation, the early March failure of Silicon Valley Bank: each of these events landed like a punch on the chin of the private credit market. And yet, “that market has just continued to stay resilient, despite the pullback in M&A,” said Sherman Guillema, managing director, capital advisory group at investment bank Lincoln International. Indeed, Brad Stewart, managing director in the debt advisory group of investment bank Capstone Partners, said his firm had two private-credit deals in the market when the news of Silicon Valley Bank hit. None of the lenders evaluating those deals put pencils down, he said, and both deals remain on course to close.

Source Talks ep. 39

On this episode, Mark Gartner of RLH Equity Partners talks about RLH’s people-focused investment strategy and research-driven sourcing mechanism.

Secondary Buyers Emerge as Big Contender for Deals

With deal flow scarce, the last thing PE firms need is a new, aggressive competitor for transactions. But that is what they’re getting from secondary buyers. First consider where deals are coming from these days. By seller type, private equity firm themselves accounted for 24 percent of platform acquisitions last year, coming in second place behind private companies, according to data gathered by SPS by Bain & Co.